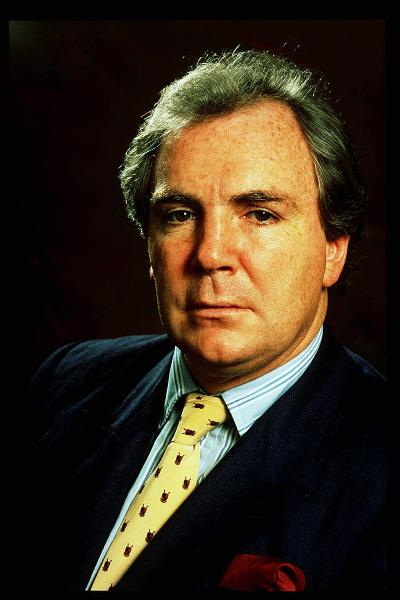

Tony O'Reilly, the businessman often said to be Ireland's first billionaire, made his career in food, media and other industries in Ireland and internationally. In 2009, as the global recession bit, his hugely successful career began to unravel with the announcement that the Irish company Waterford Wedgwood, of which O'Reilly was chairman and lead shareholder, was to be placed in receivership. O'Reilly had put hundreds of millions of his own money into the company, and its failure meant this money was lost.

But his next battle was even more significant: the businessman Denis O'Brien was challenging O'Reilly for control of Independent News & and Media, the company O'Reilly had built into a global media empire, which was now in serious financial trouble.

He would ultimately become embroiled in a humiliating legal case over his large bank debts, and be forced to sell his principal homes, art and all other valued assets.

0 of 5

‘Seen as the safest company in town’

In spite of the immensity of the Waterford Wedgwood collapse, O'Reilly did not have time to wallow in self-pity. He was still full-time chief executive of Independent News & Media, and its crisis was deepening.

At the end of January he admitted that efforts to sell APN, a newspaper publisher in Australia and New Zealand that Independent News & Media owned, were being abandoned. Instead, other "nonstrategic" assets were to be sold, although this would produce only a fraction of the money that the sale of APN would have raised; belatedly, O'Reilly's cherished London Independent was officially for sale.

Efforts were to be made to sell a new bond to replace one for €200 million that was due for repayment later that year. No final dividend would be paid to shareholders from the 2008 profits, saving Independent News & Media (INM) the €60 million it had been projected to cost.

That was a seminal moment. As recently as November 2008, despite the shortage of funds, O’Reilly and other shareholders had benefited from the payment of an interim dividend; in his case it amounted to more than €10 million. “You invested in INM for the dividend,” says one key executive. “It was viewed as the safest in town, because O’Reilly needed it, so he’d always pay it. Nobody ever thought the money wouldn’t be there to pay it.”

The loss of dividend income would be devastating to O’Reilly. In the decade up to 2006 he had pulled an average of €14 million a year in dividends out of Independent News & Media. In 2007 he had taken a record €30 million. He needed that money to pay his bills.

O’Reilly always believed that things would come right for him if he waited, because they always had. But he had left it too late this time. “Too often he spoke about how he’d done things 20 years ago, and 30 years ago, and we’d have to say, ‘But that was then and this is now, and things have changed,’ ” says one of his loyal executives. The end was imminent.

The businessman Denis O’Brien was now a major shareholder in the group. The company’s deteriorating financial position had led to a halt in hostilities with O’Brien some months earlier, despite two years of angry words and public squabbling. O’Reilly’s son Gavin O’Reilly, Independent News & Media’s chief operating officer, felt he was working well with O’Brien and, particularly, his adviser Paul Connolly.

Gavin didn’t want to continue simply as a go-between flanked by his two major shareholders. An arrangement was made for Tony O’Reilly and O’Brien to meet for the first time since the latter had become an Independent News & Media investor.

‘A younger, more determined enemy’

The meeting took place in late February 2009, the day of an Ireland v England rugby international at Croke Park that both men were attending. O'Brien refused to go to Castlemartin, O'Reilly's Co Kildare estate, for talks, and a suggestion that they use the house of a mutual friend, Ray McLoughlin, was nixed when he said that he had decorators in and that it was unavailable.

Instead they met at O’Reilly’s Dublin town house, on Fitzwilliam Square. O’Reilly had been involved in many confrontational meetings during his career, and he had usually come out on the winning side. This one threatened to be different, however. A younger, more determined, more unpredictable and seemingly ruthless enemy threatened him – and had the money to carry out that threat. O’Reilly was determined not to cede ground.

The meeting did not start well. O’Brien felt that the chair he was offered was lower than O’Reilly’s, and deliberately so. New seats, of equal height, were brought in.

O’Reilly had a table set for lunch, full of Waterford and Wedgwood products, but O’Brien was not for eating. Nonetheless, O’Brien says that the meeting was cordial. “Tony kept on asking me why I bought the shares in the first place.” That was hardly the point, given the situation in which the company found itself. “I suppose he felt we were aggressive in our demands, but the business was on the brink of receivership.”

No agreement about Independent News & Media was reached as they debated its financial condition and management, other than that they would meet again after the match, this time in the company of Gavin, Paul Connolly and Ray McLoughlin. This was when the most serious blow was delivered.

O’Brien indicated that if O’Reilly did not retire he would demand an extraordinary general meeting to remove him. O’Reilly could not be certain of winning such a vote, given the strength of O’Brien’s voting power and the possibility that other shareholders would come to the same conclusions as O’Brien and the lenders about O’Reilly’s responsibility for the perilous state of Independent News & Media’s finances.

Resigning now would offer some cover against indignity, but losing a vote publicly would be humiliating. And the campaign before an egm vote would result in even greater scrutiny of the company’s finances and, probably, an even greater fall in the share price, further eroding what was left of O’Reilly’s assets. It might even have tipped Independent News & Media into examinership or receivership.

O’Brien made it clear that he had the resources to withstand such an eventuality and that he considered O’Reilly did not. It was a game of poker, and although both held poor hands, O’Brien’s was the better.

O’Reilly was bewildered by what he saw as O’Brien’s aggressiveness. He was willing to concede on certain points but did not want to capitulate. One thing he certainly didn’t want to give up was his seat on the board; if he had to relinquish his role as chief executive, he wanted to remain as chairman. Nor did he want to give O’Brien’s representatives seats on the board. As he saw it, that would be surrender. He suspected that the offer of their involvement as partners on the board was something of a Trojan horse.

The meeting broke up without agreement, but O’Reilly now knew, if he hadn’t before, that his place in “his” company was nearing its end. “He had such a grip on the business as CEO, and a weak chairman in Brian Hillery, and he controlled every aspect of the decision-making process,” that he had to go, O’Brien says, explaining why he was so determined to remove O’Reilly. “They thought it was News Corporation they were running.”

‘This day was totally different’

Within two weeks O’Reilly’s sons and the board put him under further pressure to step down, not just as chief executive of Independent News & Media but also from the board entirely. There was speculation that banks had made his departure a condition of refinancing the business, but that wasn’t the case. The pressure had come from within, as those around him realised that further resistance was futile and that they were at risk of losing everything.

One of O’Brien’s criticisms was that, “unfortunately, Tony O’Reilly did not listen to his board, his advisers or his friends”. O’Reilly still had to be persuaded, but those were the people who were belatedly exerting the necessary pressure.

O’Reilly spent March 12th at Citywest, Independent News & Media’s corporate HQ (and main printing plant) on the edge of Dublin, discussing plans with Gavin and Tony jnr, board members and executives, demanding that they not surrender. He did not receive encouragement. It was an emotional and difficult day for all concerned.

He went home to Castlemartin to think and later rang the boardroom, where all of his executives and available directors had assembled. He was put on speakerphone. O’Reilly asked each person in turn if he agreed that he should step down and allow O’Brien’s nominees on to the board.

He was stunned by the outcome. “It had always been his show, and if you didn’t like it you got off the board. This day was totally different,” one participant says. Reluctantly, each replied that he, and they, had no choice but to say that he should go. In one of the most difficult moments of his life O’Reilly gave in – albeit arguing that they would all regret this – and hung up the phone to be left in his study with his thoughts.

The bitterness he felt would never really leave him, even if it ebbed in time.

‘It’s a fairly humbling position’

O’Reilly could not admit to this disquiet publicly, however, not when he was still a major shareholder dependent on a recovery in the stock price, not when Gavin was now chief executive and had to work with O’Brien’s people, and not when to do so would be a public admission of failure.

Gavin told Paul Connolly about the impending resignation, and once agreement on Gavin’s elevation as part of the deal was confirmed, they began writing statements for the stock market. This had to be handled gracefully.

The fiction had to be maintained that O’Reilly had chosen his own time of leaving, that he had not been forced. Part of this involved giving him the title of president emeritus and allowing him to step down the following May 7th, his 73rd birthday, rather than immediately. “I welcome the changes to the board and the appointment of Gavin O’Reilly as group CEO,” O’Brien said. “I would like to thank Tony O’Reilly for his long-standing contribution to the company. I welcome Tony as president emeritus and also take this opportunity to wish him well on his retirement.”

Gavin also put his best foot forward, dismissing talk of ongoing tension with the O’Brien faction. Gavin conceded that both sides had “thrown grenades at each other” and that this had been foolish. “I’m very happy to say that it’s water under the bridge. We’ve been working with and talking to Denis and Denis’s colleagues for quite some time now. This is a triumph for common sense and in the interests of all shareholders.”

As for himself, “It’s a fairly humbling position I find myself in, with very big shoes to fill. I have the endorsement of both Tony O’Reilly and Denis O’Brien, which is pretty good, especially when they represent 55 [sic] per cent of the company.”

A most unlikely alliance

The power shift at Independent News & Media was enormous. Gavin’s promotion was O’Brien’s only concession to O’Reilly family interests. O’Reilly did not share his son’s optimism about developing a relationship with O’Brien but saw it as his best shot of retaining power by proxy, no matter what Gavin might say about his own independence.

O’Reilly had a line he often liked to use in interviews and speeches. Whenever two great rivals in business ended up helping each other he would joke that it was the most unlikely alliance since the Stalin-Hitler pact. Now he was part of such an arrangement.

Gavin was put in a near impossible situation, notwithstanding his efforts to put on a brave face or newspaper profiles that argued that his time had come by right. Despite the relationship he had established with Connolly and all of the nice words agreed for press releases and public statements during the transition of power, Gavin knew he would remain answerable to his father as one major shareholder and to O’Brien as another, while also having to fulfil his legal and ethical obligations to all shareholders, staff and creditors, including the banks.

O’Reilly said it had been his pleasure to have worked with a range of highly talented and hugely committed directors and colleagues at Independent News & Media. “My appreciation of them is undiminished by time. Together we have expanded this Irish newspaper group and enshrined a fiercely independent editorial policy that is widely respected across the world.”

The company’s shares, down more than 94 per cent in the 12 months before the accord, went up when the news was released, but Independent News & Media’s market capitalisation was just €142.67 million, and the business had nearly 10 times that in debts. But what many overlooked at the time was the significance to O’Reilly of losing his income as chief executive – €1.4 million the previous year and as much as €4 million in 2006 and 2007 – on top of the earlier loss of dividends.

‘Yes, he loved the feeling of power’

If O’Reilly had suffered a devastating blow because of the loss of income, he also suffered a psychological one from the loss of position. One of the people closest to him, speaking anonymously, says that O’Reilly had been “exemplary in his performance as a press baron. He felt strongly that being the chairman of INM was a public role, albeit an unelected one, and as an unelected one it behoved him or whoever ran INM to do so while exercising an appropriate duty of care. He was never a Murdoch, never somebody who actively wanted to change governments. Yes, he loved the feeling of power, the proximity to it, the interacting with it, but he didn’t seek to exercise it.”

It was a contention with which many were likely to argue, both north and south of the Border. "If you look at the treatment of, for example, John Hume by the Sunday Independent during the early stages of the peace talks in Northern Ireland, it was an absolute disgrace," Denis O'Brien says.

"Here was a man who had devoted his life to the pursuance of peace on the island, and he was vilified. It took a huge toll on his health. There were many others who were subjected to poisonous attacks. The coverage of Liam Lawlor's death by the Sunday Independent was one of the lows of Irish journalism in my lifetime. And what was done about it? Absolutely nothing. No one was fired, no one was suspended. I think it is reasonable to assume that the board and management condoned such conduct by their lack of action."

O'Reilly's performance during the crisis of 2008 and early months of 2009 was more of the kind that might have been expected from a chairman than from a chief executive of a besieged company. Much of the heavy lifting was left to Gavin and, as finance director, Donal Buggy.

“It wasn’t that he was unaware of what was going on and was not hands-on day to day,” says one insider. “He was, very much so, being aware of every move and negotiation, and he had all the details. But he didn’t go to the meetings with the banks, other than a few. I remember him being at one with AIB, and he was clearly very uncomfortable. It was a little bit humiliating for him at this stage of his life to be somewhat beholden to those banks. It was a matter of pride.”

Until his departure in 2009 “he always maintained his equilibrium and his sense of humour, even if there were ever more regular dark moments. No matter what else was going on, at Waterford or elsewhere, he was always able, always continued to function, and with considerable good grace.”

Some of his former executives still defend him, although for various reasons they don’t want to speak publicly. “Everything is perfectly clear in hindsight. There are plenty of people who say now that the business was too highly geared, but I don’t remember many people saying that before 2008. Denis O’Brien clearly didn’t think so or else why would he have spent so much money buying shares in the company?” one says.

Another of O’Reilly’s executives says that by gearing the company heavily with debt he had left no wriggle room for things going wrong. He had then worsened the situation for the company by failing to refinance loans early enough, by having it buy back its own shares and by continuing to pay generous dividends when the priority should have been to cut debt.

“The share buyback was so myopic, and afterwards Tony blamed other people, which was so unfair,” one executive says.

A number of interviewees for this book, all connected to Independent News & Media, believed money that had been wasted on Waterford Wedgwood could have been used to save O’Reilly’s position at INM. In the end neither could be salvaged. The what-ifs are purely theoretical, because by 2009 O’Reilly’s carefully built position, wealth and reputation had been largely erased.

O’Reilly’s grace under pressure

When, as part of the enforced settlement with O’Brien, O’Reilly set his retirement date for his 73rd birthday, the deadline meant that he would not enjoy a valedictory final agm of shareholders, as he had at Heinz, where he had spent almost 30 years, becoming chief executive and, later, chairman. But then there was little to celebrate this time.

After March’s enforced abdication he attended just one final Independent News & Media board meeting, where he had to greet O’Brien’s three nominees. It was a great demonstration of grace under pressure. O’Reilly made no reference to the circumstances in which he had been removed and instead was most generous in his welcome of Leslie Buckley, Paul Connolly and Lucy Gaffney.

He referred favourably to Buckley’s previous work on his behalf as a consultant at Waterford Crystal, in the 1990s, and to the rugby activities of Connolly’s father going back to his time at Belvedere College. He complimented Gaffney on bringing some glamour to the boardroom.

She was not insulted by what other women might have interpreted as sexism. “If it had been Gavin who’d said it I would have objected, given how hard I’ve worked to get to where I am,” she says, “but from Tony it was what somebody of his age saw as a compliment and courtesy. I took it in that way, and it didn’t annoy me at all.”

Once the business of the meeting was done, O’Reilly, with great sadness, took his leave of “his” company.

Independent News & Media didn’t just have enormous debts. It had also committed to repay sizeable chunks of them very soon. The most important immediate debt was one of €200 million falling due on May 18th, just 11 days after his resignation. Another €50 million was due in September, as well as a further €340 million tranche and another €200 million a year later, in 2010, before even bigger amounts in 2012.

That was Gavin’s issue to deal with, even if it was going to be essential to his father, too. O’Reilly had his own financial issues to deal with simultaneously. As well as personal debt, he was having severe cash-flow problems.

His answer was to borrow, almost as if in the hope that something would turn up. Remarkably, he was facilitated. In the summer of 2009 he borrowed €4 million from AIB, offering as mortgage security his old holiday home in Glandore, in west Cork, which he valued at €4.3 million, as well as the rights over a balance of €278,000 in the account of a company he owned called Brookside.

Crucially, he also gave the bank a personal guarantee, giving it the right to pursue all of his assets should he default. It was a remarkable decision. That O’Reilly had decided his situation would be resolved by further borrowing emphasised not just that he was willing to gamble but also that he had to gamble, that he had no other cash. That alone should have alerted AIB to the dangers involved in advancing him money.

Of course, that AIB – existing only because of the generosity of the State’s infamous 2008 guarantee to all of its creditors, and in need of a capital rescue from the government amounting to an enormous €21 billion – was willing to advance such a large sum to a 73-year-old based on a property mortgage was just as extraordinary.

It wasn’t the only personal loan that O’Reilly took out that year. Three months later he borrowed the same again from ACC Bank (owned by the Dutch Rabobank) by remortgaging his Fitzwilliam Square town house and Castlemartin and giving it first call over those properties.

But the really big loan came from Bank of Ireland. It gave O’Reilly €27 million in December 2009, allowing him to participate in an emergency fundraising among Independent News & Media shareholders. This brought O’Reilly’s total borrowings by the end of the decade to nearly €300 million, spread across AIB, Bank of Ireland, IBRC (formerly Anglo Irish Bank), ACC Bank, Ulster Bank, Trust Bahamas, EFG, Lloyds TSB and Mellon Bank of the United States.

The loan from Bank of Ireland was essential: without it O’Reilly’s share in Independent News & Media would have dropped dramatically. But that it was necessary was only because of the failure of O’Reilly’s biggest effort in 2009 to rid himself, and INM, of O’Brien.

O’Brien is spooked

Gavin had taken to his chief executive’s role with gusto, but the honeymoon was extremely short. It wasn’t just a case of looking over his shoulder to see when O’Brien’s mood would change again; he faced an immediate crisis common to all shareholders: the €200 million in bonds that had to be repaid on May 18th.

Assets had to be sold to meet the debts, and as quickly as possible. Tony O’Reilly was going to have to look on as the empire he had spent 35 years building was dismantled. The only question was how much of it would have to go, although the prices were important, too.

The company had left it too late not only in talking to the bondholders but also in raising cash from asset sales. As it was a known distressed seller, and one selling into a deep recession, it would probably be able to attract only disappointingly low prices for its assets – if it could offload them at all.

First to be offered for sale were INM Outdoor, which was a South African advertising business, and INM’s minority shareholdings in Cashcade, a casino-software firm, and Verivox, a price-comparison company. Independent News & Media hoped to raise €150 million, but it quickly realised that it couldn’t get any of the cash before the third quarter of the year. Its 20.7 per cent stake in Indian newspaper interests was unofficially put up for sale. Most importantly, the efforts to sell the 39 per cent share in APN, announced in January, failed.

O’Brien was spooked by all of this, sharing executives’ belief that it was in any case entirely wrong to sell APN. O’Brien began to worry even more about Gavin’s ability to formulate and then execute the right strategy to rescue INM from its crisis with bondholders. “I don’t believe in having media outlets just for the benefit of journalists and great writers,” he told journalists, sending a shiver through their collective spine.

O’Brien described the chances of refinancing Independent News & Media’s bonds as less than 50:50 and began agitating publicly against bondholders’ demands for full or nearly full repayment. “If they think Denis O’Brien is going to write a cheque to the bondholders, then they are smoking dope,” he said of himself.

‘I will destroy you and your father’

But sorting out the bondholders was not the only issue. The further bank borrowings of €

50 million due for repayment that September were senior debt, meaning that they had to be repaid first, before anything went to bondholders, in the event of a default. The bondholders agreed to a standstill, suggesting that they were confident the other lenders would not pull the plug on INM – not yet, anyway.

At the end of August 2009 Gavin hosted a press conference at which he admitted that falling advertising income had led to a 22 per cent drop in Independent News & Media’s overall revenue in the first half of the year, to €608.8 million.

What Gavin did not publicly reveal at this stage – although details were to appear in two newspapers the following Sunday – was that he and O’Brien had had a rollicking row the evening before the figures were published.

Gavin had been in his office at Citywest when a call from O’Brien, who was holidaying in Ibiza, was put through. It was a three-way conversation, although the third participant, Connolly, said almost nothing.

They started with what had transpired at a previous board meeting, on August 19th, which had endorsed, by majority vote, the sale of the South African outdoor-advertising firm, raising €98 million, despite objections from O’Brien’s representatives that it was worth more – and indeed should not be sold at all.

O’Brien, who had not been present at the meeting but had been told about it by his directors, described the debate as “the lowest of the low he had ever seen at a plc”. He claimed that the “O’Reilly directors” had “ganged up” on his three nominees, and he took particular offence at the perceived treatment of Gaffney.

O’Brien told Gavin that in March they had “agreed to be aligned” but that Gavin’s actions constituted a “solo run”, which meant he had “broken the agreement”. When O’Brien told him he “needed to start to consult with shareholders”, Gavin replied that he did and that he was surprised to hear the complaint about solo runs for the first time the previous week. Gavin said management was merely trying to find a solution to the crisis. It was like waving a red rag at a bull.

Gavin reported afterwards that O’Brien became more “agitated” and said that “things needed to change” and that, unless they did, he’d call an egm of shareholders “tomorrow”. Gavin told O’Brien that this was his right but said that O’Brien became more aggressive in response to this reasonableness. As Gavin continued to protest, O’Brien told him he “wasn’t capable of delivering a deal” with the company’s bondholders.

Then came the most inflammatory comment of all: O’Brien told Gavin that, if he wanted a fight, “I will destroy you and your father, and I will go after everything.”

Although shaken, Gavin had the presence of mind to write down, as soon as the call ended, what had been said. He had not taped the telephone conversation – to have done so without consent would have been illegal – even though he was to be accused of that later.

Gavin took advice about what to do. He was told not to refer to any of it at the following day's results, to carry on as normally as possible. But the story was then given to both the Sunday Independent and the Sunday Times newspapers.

In response O'Brien told the Sunday Times that the crisis at Independent News & Media "has been escalating for years" and that the banks, bondholders, investment community and staff had seen it coming. He claimed that people with responsibility "took no action".

O’Brien says now, “I think Gavin was rather selective in his disclosures to journalists during this entire period. Mysteriously, Gavin was able to remember, word for word, conversations which he was able to transcribe after having these conversations.” He also explained how and why he had lost confidence in Gavin. “I always said he was a spoofer and a silver-spoon merchant.”

Gavin O’Reilly’s terrible position

O’Brien was determined to expose Tony O’Reilly’s soft underbelly, calling for an egm to “address the serious concerns relating to the company’s corporate governance and to seek to avoid further destruction of stakeholder value”.

He wanted shareholders to call for a “detailed schedule” of all board-member expenses since the start of 2000, sensing that disclosure of the information would considerably embarrass the O’Reillys.

O’Brien called for a vote to cancel the €300,000 annual payment to Tony O’Reilly, which had been agreed only five months earlier, for his titular position as president emeritus.

Gavin O’Reilly was in a terrible position. He was in regular contact with his father, in his capacity as a major shareholder, about the financial restructuring with the banks and bondholders, because he had to be able to convince all of INM’s lenders that the O’Reillys and O’Brien were working together to save the company.

As chief executive, Gavin was legally required not to favour, or be seen to favour, one shareholder over another, but his father’s prior role in the company and O’Brien’s insistence on targeting him complicated matters dramatically and made such discussions with his father more difficult.

The “I will destroy you” comment caused no extra concern to the O’Reillys, however; they were working on that assumption anyway.

The penny drops for O’Reilly’s banks

The eventual deal with the bondholders saved the company but was still humiliating for Tony O’Reilly. The bondholders were to get 46 per cent of the ordinary shares in Independent News & Media in return for writing off €123 million of the bonds’ outstanding principal. There was then to be a rights issue among existing shareholders – it raised €94 million – with this money being used to pay off the bondholders.

The new shares were sold for 5c each, compared with the existing 27c share price. Both O’Reilly and O’Brien invested fully in their rights. This cost Tony O’Reilly about €27 million, which he borrowed from Bank of Ireland. It left O’Reilly with 14.7 per cent of the shares in the newly reconfigured company and O’Brien with 13.8 per cent.

Weeks of further acrimony followed, especially at egms called either by the board, to approve measures Gavin wanted to implement, or by O’Brien, to try to stop them. The O’Reilly-dominated board received the backing of shareholders in them all.

Within weeks of seeing off O’Brien’s challenge Gavin admitted that Independent News & Media would not meet its projected operating profit after all. At the end of October it reduced its forecast to €170 million-€190 million. It was the third reduction in six months.

The London Independent newspapers were sold to the Russian businessman Alexander Lebedev, a former KGB agent who already owned the London Evening Standard. He paid just £1 for the titles. More importantly, he agreed to pay £9.25 million, or about €12 million at today's exchange rate, of the existing debts and assume "all future trading liabilities and obligations".

It would be considered a good deal in retrospect, as the Independent made an operating loss of £12.4 million in 2009, as circulation fell below 100,000; Lebedev lost a further €40 million in his first three years of ownership.

As Gavin continued to try to sell INM assets to pay off debt, his father’s personal position got worse as he tried to deal with his own debts of nearly €300 million. The penny was dropping for many of O’Reilly’s banks that all was not as they had assumed.

O’Reilly’s lenders were becoming anxious about his ability to repay his debts. His lack of cash flow and saleable assets was dawning on them. He was being asked when he would be able to make repayments, but he was unable to provide the required answers. Interest was mounting, continually increasing the size of his debts.

O’Reilly turned to Bernard Somers for help, as he had done many times over the past 20 years. An insolvency specialist among other things, Somers had done a remarkable job on behalf of Larry Goodman when the beef baron got into enormous trouble in 1990 after a period of reckless stock-market investments, property punts and failure to recover money owed from Iraq left him with debts of more than IR£500 million. Somers had been a director of INM since 1998, having previously worked as a consultant to the group.

Somers visited O’Reilly’s nine banks and made a plea: he wanted all to consent to a standstill agreement that would give O’Reilly three years to sell as many assets as possible to cover his debts, without the fear of a bank suddenly moving to enforce a debt.

Keeping the arrangement secret would not just spare O’Reilly’s blushes: it would also stop the fall in the value of those assets if buyers realised his financial distress.

Many of the banks were pragmatic: they believed that the assets would be worth more in a recovering economy and that it was worth the gamble of a wait. Some also believed that O’Reilly’s business career and contribution to Ireland’s economic development had earned him the right to time.

Somers got his client the necessary agreement. But this bank debt would come back to haunt Tony O’Reilly.

This is an edited extract from

This is an edited extract from The Maximalist: The Rise and Fall of Tony O’Reilly

,

published by Gill & McMillan next Frida

y.

Irish Times

readers can buy e

arly copies

for

€

19.99, reduced from €27.99, and with free shipping, through our partner

[ Kenny’s bookshopOpens in new window ]

. The first 100 of these copies are signed by the author

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}