Noticed the price of your cup of coffee going up ? Or your visit to the hairdressers? One of the most controversial moves in the last Budget was the increase in the 9 per cent VAT rate, amid warnings that it would hit the hotel and restaurant sector and tourism.

It is too early to judge whether it will – but what is clear is that the bulk of the rise is being paid by consumers. The evidence, in recent inflation figures from the CSO, shows an extraordinarily quick pass-through in the VAT increase to consumers immediately it took place in January.

The same would likely happen in the case of a lot of the tariff – or import tax – increases which would take place in a no-deal Brexit, which would be immediately evident in Irish supermarkets. Evidence from the tariffs imposed by President Donald Trump in 2018 are that they passed through almost entirely to the US domestic economy.

The background

Who ultimately pays for a tax increase – or a new tax on a consumer product or service – depends on the market involved and how supply and demand react to higher prices.

Excise taxes on tobacco are often used as an example of an area where demand remains high, even as taxes are hiked again and again. This means producers pretty much always pass on the rises automatically to smokers. The same tends to happen for alcohol price rises. The taxes – particularly on tobacco – are justified by their public health impact, and the numbers smoking have declined progressively over the years. But the willingness of many consumers to keep buying even as prices soar means they are also a juicy source of revenue to the exchequer.

Economists refer to this “who pays?” debate as a question of the “incidence” of the tax. It can also be affected by the profitability of the producer, who can find it difficult to absorb a higher tax if margins are tight.

The 9 per cent VAT rate was introduced in 2011 as part of a jobs initiative, reducing the rate from 13.5 per cent for a range of sectors including hotels and restaurants, newspapers, personal services like hairdressers and leisure services like cinemas, museums, theatres and some sports activities. Most of the sectors were moved back to 13.5 per cent in the last Budget, though the lower rate on newspapers was retained.

A Department of Finance study beforehand suggested that the lower rate may have had a short-term impact on employment in the sectors involved, but that their recovery and growth was mainly due to rising incomes across the economy. The report also suggested that many companies in the 9 per cent rate sectors – in particular hotels and restaurants– " have scope to absorb a higher VAT rate via the healthy profit margins within these sectors." The study showed sharply rising profitability and improving margins in recent years, particularly in hotels.

Revenue data shows that the bulk of sales qualifying for the 9 per cent rate were, not surprisingly, in hotels and restaurants, according for over two-thirds of the total collected.

Not all sales in these establishments were at the 9 per cent rate – it accounted for 76 per cent of sales in hotels and 88 per cent in restaurants. Alcoholic drinks and soft drinks, for example, as charged at higher VAT rates.These variations – and the fact that other costs like wages may be putting pressure on prices too – mean it is not possible to judge exactly how much of the VAT rise from 9 to 13.5 per cent was passed through.

But the evidence is pretty clear, with sharp increase in prices in January and in some cases further increases in February.

What happened

The evidence is in and it shows that the VAT hike was, in general, not absorbed by many of the players involved but flowed straight through to prices. The one exception is accommodation services – room in hotels and guesthouses – where the evidence is not clear.

In most of the main sectors involved prices jumped immediately the VAT rate changed in January. You could argue whether firms were taking advantage of a strong economy and might have absorbed the rise.

Or whether tight margins left them with no alternative. Even within sectors there were, no doubt differences. A profitable hotel in central Dublin, for example, would have different economics than one in a small town in the Midlands.

But in general, prices rose. Gerard Brady, head of tax and fiscal policy at IBEC, said he was not surprised at many of the rises.” I’ve said before that Irish restaurant and cafe margins weren’t big enough to do anything but pass on the increase in the 9 per cent VAT rate to consumers,” he said. The figures “showed as clear an example as you could see of price-pass-through,” he said.

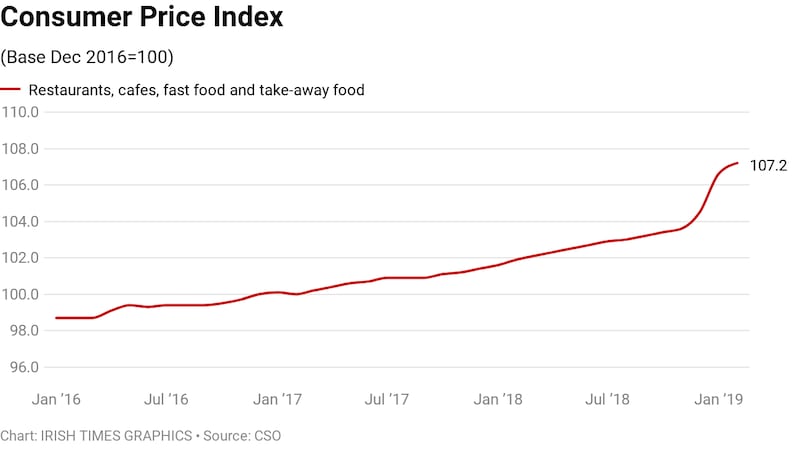

In the restaurant sector the evidence is striking , with a 2 per cent rise in January in prices compared to December and a further 0.6 per cent increase in February. This left prices 5.2 per cent up one on year earlier. A separate category, combining restaurants and hotels, shows a 0.7 per cent rise in January and a 0.8 per cent increase in February, leaving prices up 3.6 per cent year on year.

It seems food and beverage prices followed the VAT rate higher, but room rates have not done so. Looking at accommodation prices in hotels and guest houses on their own, there was a prices fall in January ( which usually occurs for seasonal reasons ) and a bounce back in February, so it is not clear what the impact of the VAT rise is here.

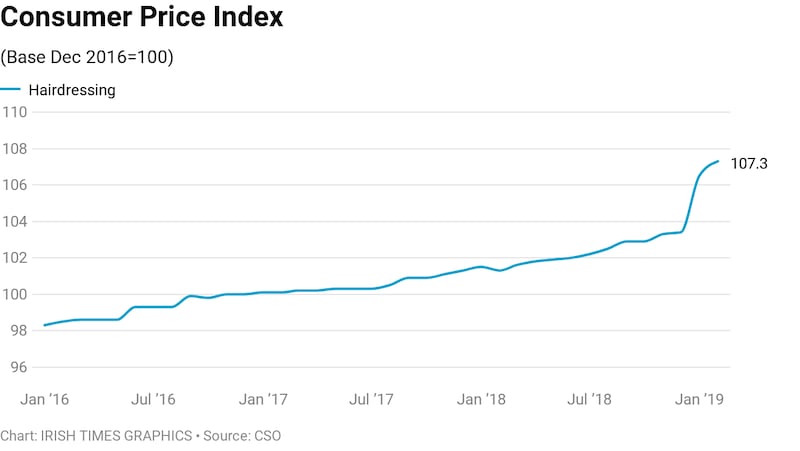

There is clear evidence of price pass through in hairdressing, a lower margin sector according to Revenue data, where prices rose by 3 per cent in January compared to December and a further 0.8 per cent in February.

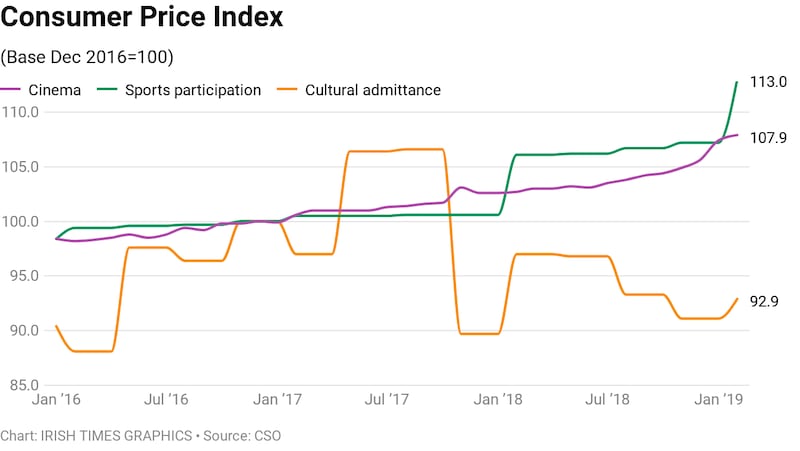

This left prices 5.9 per cent up on one year earlier. Prices for cinema , up 5 per cent year on year in February, also seem to show the VAT impact. However for cultural admission to museums and sports participation – the likes of golf green fees – the evidence is more mixed, though both showed significant price rises in February.

In summary, the rise appears to have been pretty much generally passed on for food and drink in restaurants and hotels and for personal services like hairdressing. For hotel rooms we will have to wait and see, but perhaps higher margins in this area allowed the rise to be absorbed by some.

So what is the Brexit angle?

There’s always one these days. Brexit will, sooner or later, end the current trading arrangements between the EU and UK. Typically countries in different trading blocs impose tariffs, or import taxes, on imports from each other – for example the EU puts tariffs on many goods coming from third countries.

While many of these are low, they are higher in traditional areas like clothing, textiles, some engineering products and, particularly, food. Tariff on UK imports here – and Irish exports to the UK – would follow a no-deal Brexit. They could also be imposed if in future, after concluding a withdrawal agreement, the EU and UK do not reach a future trade deal, or agree one which leave some tariffs in place.

Tariffs are taxes which fall due to be paid by importers to the exchequer of the State imposing them. However who pays the economic burden can vary. It can be the exporter, via a lower price, the importer via lower profits or the final consumer, via higher prices. (There may also be wholesalers or manufacturers in the supply chains affected.)

Historically evidence has varied on who pays the economic price, depending on issues such as the size and thus importance in the market of the importing country and the economics of the product market involved.

But often, the consumer pays. A major study of the tariffs imposed by Mr Trump in 2018, mainly on steel and aluminium and Chinese products, showed that pretty much all the price increase was passed on to importers and US consumers.

The study, by the Centre for Economic and Policy Research, said that US domestic consumers ended up paying the full price and that extra revenue to the US exchequer did not compensate for this and for other wider economic losses from the tariffs.

For a small country like Ireland, the odds are that tariffs would pass straight through to consumers in most cases. Just like the VAT increases. A study by the ESRI for the Consumer and Competition Protection Commission estimated that the costs from higher tariffs and other trade barriers following a harder version of Brexit could increase prices to Irish households by around €900 to €1,350 a year, with big increases in many consumer food products.

Poorer households, who spend more of their income on basic products, would suffer the post – a point also reflected in many other international studies. Tariffs, especially in a no-deal situation, would also be likely to disrupt supply lines and lead to some producers being priced out of the Irish market, just as some Irish exporters will be priced out of the UK.

The bottom line

The bottom line , with taxes and tariffs, it not who makes the payment to the exchequer. It is who ultimately pays the bill. There is rarely a straight answer – for example, do employers pay lower wages because they must also make social insurance payments? And often the impact of tax increases and cuts is different. However looking at the VAT rate rise and the recent research on tariffs, it is clear that the consumer if often the one in the firing line.