A whole generation of mortgage borrowers have no experience of rising interest rates. But 2019 looks set to be the year when interest rates start to climb again, with implications for borrowers and savers and it appears the era of very cheap money is coming to an end.

The question for borrowers and savers is when the increases will start, how quickly rates will climb and what the rise means for the Irish housing market?

Here we explain why it is happening and what it will mean for mortgage holders.

Why are interest rates going to rise?

Higher interest rates slow economic growth, make lending more expensive and typically act to slow housing markets, though here there are other factors at play, too.

They are a key tool used by central banks to try to keep economies on an even keel and inflation at a moderate level, ie to avoid sharp booms and big busts.

In Ireland we have got used to rock bottom rates because of the crisis and its aftermath, but normally borrowing costs rise and fall as part of an economic cycle.

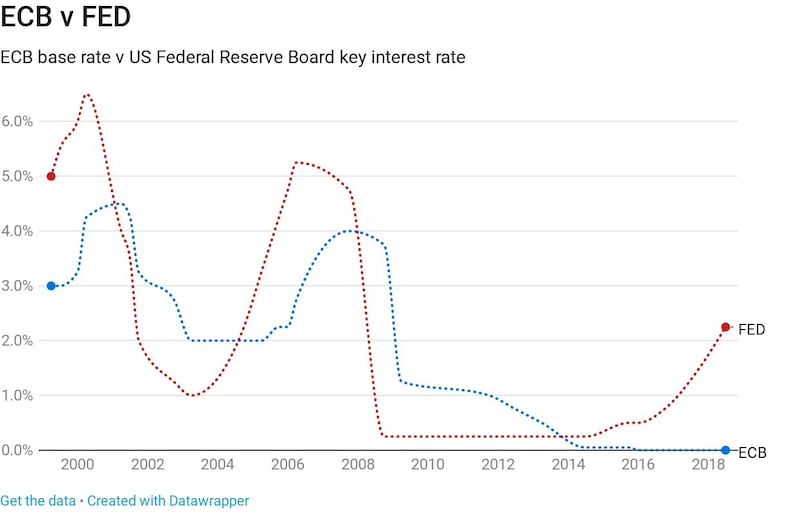

The last time the European Central Bank (ECB) raised interest rates was October 2008, when it increased its key rate by 0.25 of a percentage point to 4.25 per cent, a move seen in hindsight as a serious miscalculation.

As the euro zone economy was hit hard by the financial crisis in subsequent months, the ECB was forced to reverse course, reducing rates in October and gradually cutting them to zero over the subsequent years, where they have remained ever since.

Rates in the US and UK have already risen well off the floor over the past couple of years and Europe looks set to follow. All the main central banks cut interest rates to try to stimulate their economies and avoid deflation during the crisis.

So bad was the crisis they also resorted to pumping cash into their economies via the purchase of government bonds, so called quantitative easing or QE.

The sequence is first for QE to end and then for interest rates to rise. Withdrawing this huge stimulus is tricky, as low rates sent money surging into other markets – such as shares and property - in search of a return.

QE in Europe is due to end in December and it looks as if the years of emergency interest rates in Europe will draw to a close after that.

However, it is worth noting that Irish banks have continually had some of the most expensive mortgage rates in the EU, despite ECB rates being set at zero. So they may have room for manoeuvre as rates start to rise.

When will interest rates rise?

The ECB says interest rates will stay where they are “through” next summer. That means its key policy meeting next September is the first time when an increase is likely to be announced.

For this increase to go ahead, the ECB will need to see reasonably strong growth in the euro zone and evidence of rising inflation.

Remember, the ECB’s key remit is to keep inflation at or near 2 per cent and the main reason it hasn’t moved rates recent years is inflation across the euro zone has remained on the floor as the bloc slowly dragged itself out of the financial crisis.

in the absence of a deal, the impacts of Brexit are almost impossible to quantify

Bank analysts say so far growth is on course to allow the ECB to plan to hike rates next Autumn.

While euro zone growth figures have been slightly below expectations, "more recently the data has started to improve and we think that we will continue to see a further pickup over the coming months as the soft patch in the first half of the year proves to be a temporary slowdown following strong growth in the fourth quarter of last year," says Garret Grogan, head of global trading at Bank of Ireland.

Current growth indicators suggest the euro zone recovery is still on course, according to Simon Barry, chief economist at Ulster Bank. With signs of wage and earnings growing, it is on course to end its policy of pumping cash into the euro zone economy via bond buying by the end of the year, he said.

However, analysts also say the final decision to press the button on a rate rise will not be taken into well into next year probably in the summer time after Brexit takes place. And in the absence of a deal, the impacts of Brexit are almost impossible to quantify.

So until then, the ECB will keep its options open.

Is a rate rise certain?

If euro zone growth or inflation slowed, it could cause the ECB to postpone its rate rise. However, it will only be a postponement. The ECB has pumped billions into the euro zone economy and now it has to start to turn off the cash tap and then move to increase interest rates.

Economic forecasting is a tricky at the best of times and with risks of a trade war with the US, Brexit and fears about the Italian public finances there are plenty of things which could sharply damage confidence and throw growth off course.

Any of the above could cause the ECB to wait until the end of the year - say December – to raise rates. The ECB has three policy setting meetings at which it could move after summer next year in September, October and December.

Of course growth could also surge ahead, as it did last year. But it would be a big step for the ECB to raise rates before next autumn and that is seen as unlikely.

Once they start to rise, how far will rates go?

This is the big question, and the one that most concerns Irish mortgage holders.

At the moment long-term interest rates on the markets suggest ECB rates might not rise beyond 1 to 1.5 per cent in the next cycle. If this was true, it would be very welcome for borrowers, meaning rates would peak at a much lower level than previous cycles.

What lessons are there from the US? The experience there shows that once rates start rising they can move ahead at a steady clip!

The US central bank, the Federal Reserve Board, first nudged up interest rates from their crisis level of around zero in December 2015, the first rise in nine years, but market turmoil then stayed its hand.

The current rate cycle started for real in December 2016 and rates have risen six times since, most recently in September. The current target rate is between 2 and 2.25 per cent.

The markets expect Fed rates to rise over 2.75 per cent by the end of next year, though the members of the Fed’s key committee see them around 3 per cent by that time. This would be well below peak interest rates of 5 per cent or more in previous cycles.

At this stage, the market is not expected ECB rates to rise this much for the foreseeable future. This opens up the prospect of a longer period of historically low interest rates, even if borrowing costs do start to move off the floor.

At the moment, says Owen Callan, analyst with Investec, the average market view is for a one quarter point rise next year and one or two the following year "and a similarly slow level of rate hikes beyond that such that the ECB is still expected to be in 1.0-1.5 per cent territory by 2023."

Barry of Ulster Bank warns expectations can quickly change and a decent economic revival in the euro zone could lead to a somewhat bigger rise in rates in the next few years.

But everyone agrees the increases will be gradual, if regular, once they start. The ECB will want to get rates back to something considered “normal,” though what normal is in the post-crash, low inflation world is now debatable.

What will this mean for bank customers?

Even if the period of rock bottom rates may be coming to an end the outlook for consumers is reasonably benign, at least for now.

Increased competition has led to a flood of new fixed-rate offers on the Irish market and variable rates may also fall as a result.

Long-term interest rates may start to rise gradually as an ECB hike approaches, which could affect fixed rate offers for consumers and businesses, but for the moment competition is driving them lower.

Those on tracker mortgages will see rates rise automatically as ECB rates increase. But it remains to be seen whether variable mortgage rates – which remain well above the euro zone average – will rise by the same amount.

We could be in the odd position of seeing ECB rates edge up but many Irish mortgage rates remain where they are or even edge down as bank balance sheets improve and extra competition enters the market, according to Karl Deeter of mortgagebrokers.ie.

Rates on offer to borrowers have been under downward pressure for some time, he points out and because of the way break fees for fixed rate loans are calculated, these currently often offer good value for new borrowers who could, if they needed, escape with little of no penalty.

Recent figures show most new borrowers are now opting for fixed rates. The calculation is different for those locked in to fixed rates for some years and now seeking to end their term early to avail of lower rates on offer. They are advised to contact their bank to get the details.

Higher rates would bring some relief for hard-pressed savers – but it would be gradual. A recent survey by EasyMoney showed the average interest rate on savings in Ireland was just 0.35 per cent.

This, together with higher than average borrowing rates, means Irish banks have some of the highest profit margins in Europe.

Savings offers should start to edge up as ECB rates rise along with longer-term market interest rates, but the process will be slow and savers will still be under pressure to accept some risk if they want to get a bigger return on their investment.

***

The bottom line is the period of rock bottom interest rates is coming to an end. It could be another year – or close to it – before ECB base rates start to rise, but rise they will. Competition may limit the impact for some borrowers and those taking out loans should prepare to pay more but it could be into 2020 before they feel the difference.