Are you feeling rich? New Central Bank figures this week showed Irish household wealth is, in total, higher than ever before. But this is yet another reflection of the property boom-and-bust cycle.

Your house is an asset – and so as its price goes up so does your wealth. But what are we worth now on this measure ? And do soaring house prices really make us wealthy?

The Irish route to getting rich has been clear enough. Take a big loan, buy a property and wait. In our model wealth is much more tied up in housing than the international average, and as a nation we also carry relatively high household debt. Household debt to disposable income has fallen rapidly in recent years, but it is still the fourth highest of 17 EU countries in the latest Central Bank figures.

Taking liabilties away from assets leaves the total of Irish household wealth at its highest ever level. In per capita terms, however, we are still a bit below the 2007 peak, as the population has grown in the meantime.

Now we face some big questions. Burdened with huge mortgages over much longer terms. what are the prospects of those buying homes now to successfully taking the “Irish” route to wealth generation

We also need to recognise that your home is a unique form of wealth and is different from assets that can fund spending or are earning income for you. Housing is “wealth” in the sense that you can live in it and enjoy it and pass it on when you die. But it is not wealth that generates income or can be “cashed in” – unless you want to trade down. And if you have a big mortgage, the ability to cash in is limited or non-existent.

The Data

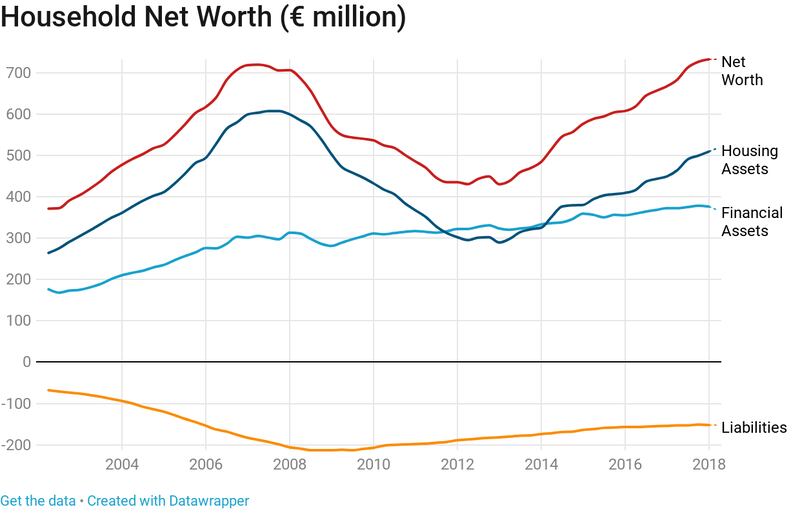

Household net worth, the value of assets owned minus liabilities – such as mortgages and other debt – hit a record €732 billion in the first quarter of this year, according to the latest Central Bank figures. This is just over €150,000 per head of population, on a rough count, approaching the previous 2007 peak of around €175,000 per houshold. Not surprisingly, the bulk of the gross assets held by people are houses, valued at €509 billion.

The notable thing is how wealth has swung since the early 2000s in line with the massive volatility in house prices. We had one of the world’s biggest property bubbles, a record collapse and one of the most rapid international recoveries in prices. With property accounting for more than two-thirds of our wealth – and around 2 out of 3 households owning their homes – this had a dramatic impact on household balance sheets.

The Central Bank figures show that the net worth of households jumped by more than 90 per cent between 2002 and the peak in house prices in 2007, rising from €371 billion to €719 billion. It then collapsed by 40 per cent to €430 billion by 2013 and has since jumped by 70 per cent to just exceed the previous record.

Since the bottom of the collapse, rising house prices have accounted for €220 billion of the overall €300 billion rise in national wealth. You would need a breakdown of mortgage figures to get behind this a bit, but the total value of household debts has fallen over the period by €30 billion, while the value of financial assets – shares, insurance policies, pensions and so on – have risen by just over €50 billion. Add these together, and you get the total €300 billion rise in net wealth since the floor.

The Comparisons

While data sets on wealth are limited, ECB figures suggest the amount of wealth accounted for by home ownership is somewhat higher here than the euro zone average – 70 per cent here versus a euro area average of around 63 per cent. This would not be surprising, given the high level of home ownership in Ireland.

That said, rising house prices have been the predominant force behind increases in household wealth across the euro area over the past few years and not only in Ireland. ECB figures show that as Europe emerged from the crash in 2012 and 2013, rising asset prices were the first thing to show up as improvements in household balance sheets.

More recently, rising house prices have been the main factor. In the past year, rising house prices have added some €5,260 per capita to average personal net worth across the euro area, the vast bulk of the total rise of €6,673 per capita over the period.

So as in Ireland, the family home is the main source of wealth for many across the euro zone. However, the sharp movements in Irish house prices mean our “wealth” has swung around by much more than the average, losing more heavily during the crash and recovering more rapidly in the meantime.

This also means Irish households remain relatively highly indebted – many took out mortgages during the boom, and those doing so now are also taking on a significant burden. This reduces net wealth, obviously particularly among younger households.

When you look at our volatile growth figures and the massive drop and then recovery in employment levels, we are truly Europe’s rollercoaster economy.

ECB figures go back to 2010 and show that from 2010 to 2015, the fall in household net worth here was €21,350 per head. Only Greece, with a figure of €20,000 is in the same ball park, though as a percentage of household spending their fall was worse. Seven euro zone countries were in the red in terms of losses in net worth over the period, with 11 showing a rise and two with figures unavailable.

The huge loss here compares to a cumulative, small, gain in per capital wealth across the euro zone for the 2010 to 2015 period of €5,719, with the bulk of the rise coming in the 2014 to 2015 period.

All of the Irish fall, not surprisingly, was due to collapsing house prices. We had, after all, further to fall, with a Bank of Ireland report in 2007 saying Irish wealth was the second highest in the OECD. Household balance sheets, it opined, were in "very good health" with assets well exceeding liabilities. The problem, of course, was that the value of assets was somewhere in cloud-cuckoo-land.

And just as the collapse was worse in Ireland, so the recovery has been more rapid. The latest ECB figures estimate that per capital net wealth here has risen by just under €29,000 in the last four years, driven by the property recovery, 47 per cent ahead of the average recovery across the euro zone and third only to Luxembourg – where a rich population benefited from stock market rises – and the Netherlands. Even adjusting for spending power here still leaves us near the top of the league in terms of gains.

However, in terms of the level of our wealth, we are close to the average. Cross-country comparisons are notoriously tricky, but the CSO 2013 data suggested we were a bit below the average in terms of average net wealth then. Given faster growth in house prices in the meantime, we have probably caught up. However this again shows our high housing cost/high debt position, as in terms of gross wealth – before debts were counted in – we were well above the average even back then and will be more so now.

The wealth spread

The latest Central Bank figures do not give any indication of the spread of wealth, so here we have to look at other data. A Daft.ie report earlier this year showed how housing wealth is concentrated in urban areas.

For example Dublin accounts for less than 1 per cent of the land mass of the country but some 40 per cent of its housing “wealth”. Interestingly some of the biggest housing wealth jumps since the crash have come in areas such as Dublin 1, Dublin 8 and Dublin 10, where massive interest from new buyers is driving up house prices. There are, it estimated, almost 4,600 “property millionaires” in Ireland, with around 15 properties worth €1 million or more sold every week.

To get more detailed information on the spread of wealth, the only comprehensive data is in the CSO’s Household Finance and Consumption Survey, the most recent of which relates to 2013. A new survey is being completed and will be published next year.

The CSO figures show 95 per cent of households have some form of “real” asset, whether family home, a farm or some property. As well as the family home, there is substantial wealth tied up in farms and investment property. Not surprisingly, the better-off and the self-employed were much more likely to own investment properties. Almost nine out of ten households had savings, though the average was just €4,500 each.

Older people and those with higher incomes, not surprisingly, are wealthier. Over-55s own almost 60 per cent of net wealth, according to the most up-to-date figures, and under-45s own less than 17 per cent. In terms of income, the top 20 per cent own nearly 40 per cent of the wealth, and the top 40 per cent of earners own 60 per cent.

Bottom line

The bottom line is that, like so many things in our economy, housing is at the heart of our national wealth - for the vast majority of people anyway. The usefulness of swinging house prices as a real measure of wealth is debatable. Interestingly, Germans, where around half the population rent, have a much lower measure of wealth than the EU average for this reason. Yet their level of savings is 80 per cent above the euro zone average. High incomes and not paying a mortgage is an alternatively way to get wealthy - but only if you don’t spend all that you earn. The Germans save 17.4 per cent of income, compared to a euro average of 12 per cent.

Rising house prices may make those who own their home feel a bit better. Economic studies show that spending rises when house prices increase, though the cause and effect here is debatable. Certainly in our boomtime people did borrow against the value of their home for investment, business or even a foreign property.

But the uniquely volatile nature of our housing market is cause for caution. We are now a relatively high-income EU country, but our wealth levels are closer to the average, and a lot is tied up in houses. Our wealth depends on our homes and this requires getting heavily in debt. And for younger people, the real question now is whether the sums add up in terms of the older generation’s life cycle wealth “play” or taking out a mortgage, paying it off and hoping to have something of greater value at the end.

* Each Thursday Smart Money looks at the big economic trends and what they mean for you.