Taxpayers generally feel they are hard done by – and wonder do people in other countries get a better deal.

Now a new ESRI study casts new light on how Irish tax bills compared to other EU countries.

By looking at where bills are relatively low here – and relatively high – it contains useful new data to guide the discussion on reforming tax and social security, which is to be examined by a new government-appointed commission.

And make no mistake, with government spending sharply higher in the years ahead, the focus is going to be where to raise more tax revenue.

1.What the researchers looked at:

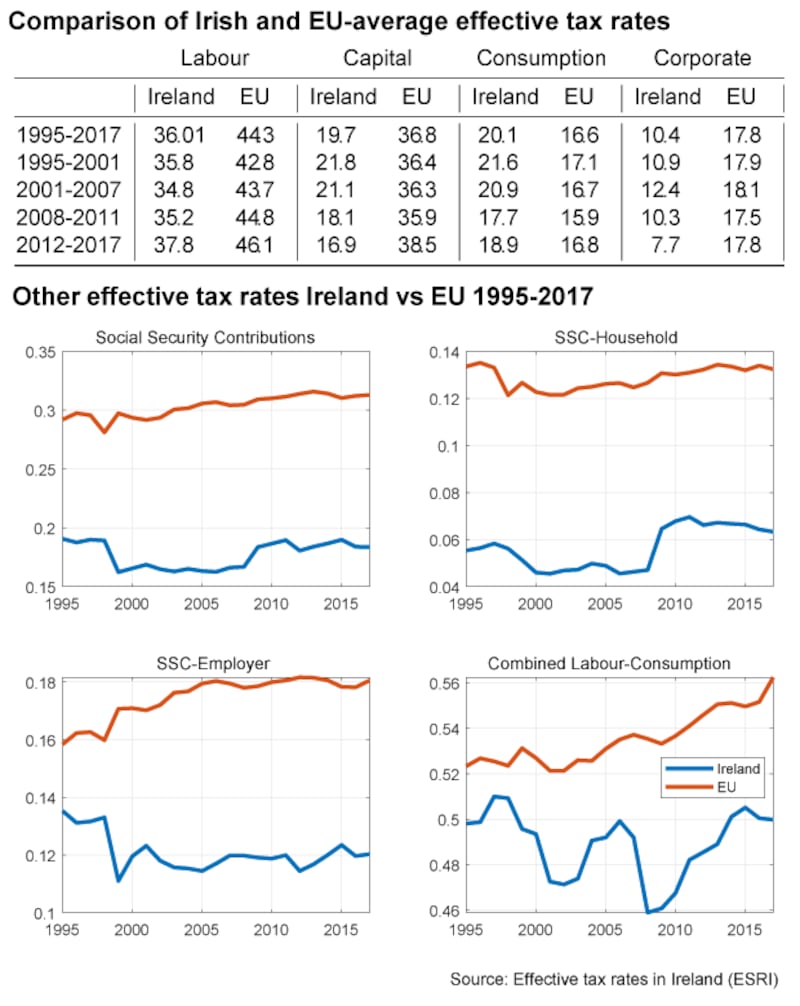

The ESRI paper – Effective Tax Rates in Ireland by lias Kostarakos and Petros Varthalitis – looks at what is called the effective tax rate.

This is the estimate of the average percentage tax take from various areas of economic activity.

They look at tax on consumption, capital, company profits and on labour and compare the take here with the EU average, looking at various periods from 1995 to 2017.

This is really useful as it shows in general where tax is raised in Ireland and how it compares to the average of our partners.

Of course there is no rule that says we must tax the same as other countries – the Irish economy has an unusual economic structure and in any case such decisions are, in part at least, political judgments.

The researchers also look at some specific areas, such as social security contributions, which are likely to be in focus in the next few years.

No one method of comparison is perfect. The research does not show the marginal tax rate on different activities, particularly work, which is the rate which applies to the next euro earned.

This is seen as important in setting economic incentives. It also does not look at how the burden is distributed – so for example how high or low income earners compare to their EU peers.

But by looking at where tax is high and where it is low or high by international standards, it does provide indicators for future policy. In this way the research sets an important context for the debate on where tax revenues should be raised in future.

2. The key finding:

As outlined in the table, the effective tax rate here differs from EU averages in some interesting ways.

The first thing to note is that tax on labour here is relatively low, with a rate of 37.8 per cent compared with an EU average of just over 46 per cent in the most recent period of 2012 to 2017.

This is partly due to lower social security charges here. We can see that tax on labour fell during the financial crisis – as taxable income dropped – and rose a bit afterwards. Remember the USC was introduced in 2011. The figures are also affected by things such as earnings and income trends over time.

The researchers also stripped out social security contributions, which they estimate are charged at an effective rate of 18.5 per cent here versus 31.3 per cent in the EU. This is a difficult area for comparison, as the benefits people get vary from country to country. Both employers and employee payments are notably lower than the EU average.

If in general we pay a lower tax rate on what we earn, we pay more on what we consume. Consumption taxes – indirect taxes like VAT and excise duties – are relatively high here.

They are charged at an effective rate of 18.9 per cent on sales, compared to an EU average of 16.8 per cent. The gap in previous years had been even more.

However, adding labour and consumption taxes together, the researchers calculate that a measure of the effective tax rate we pay here is still below the EU average.

They do this by looking at the effective tax take on incomes from labour and consumption taxes, which they say is just under 50 per cent here, versus 55 per cent in the EU on average. This is an interesting finding on the tax burden here.

Taxes on corporate profits are particularly low here. The research shows an effective rate of 7.7 per cent, compared to an EU average of 17.8 per cent.

This is a tricky area to measure, no more so than in Ireland due to the activities of multinationals and the calculation of what profit is taxable here.

The researchers refer to other studies using different methods which show that the effective rate here is higher at somewhere over 11 per cent. Nonetheless is it clear that with a headline corporate tax rate of 12.5 per cent Ireland is a low tax country for business profits.

Tax on capital is also low, partly due to the lower tax on company profits. This category also includes capital taxes paid by households in areas like capital gains tax and capital inheritances tax and stamp duties.

Again the take here is low by EU standards although the research does not look at the different components of this.

3. What does it all mean?

As part of their research the two ESRI researchers look at correlations between taxes on labour and hours worked an tax on capital and profits and business investment.

They found strong correlations in both causes, though underlined that this does not prove causation. They conclude: “This set of results indicate that the policy mix followed by Ireland is positively correlated with GDP growth and thus could be a contributing factor to the country’s strong economic performance.”

Economic research argues that taxes on labour in particular can be more economically distorting that other kinds of taxes, such as those on consumption. This is because they affect the economic incentive to work, while capital and profits taxes can lower investment. This appears to be the case looking at the data across Europe, though the researchers say that finding causation requires more research.

There are also fairness issues with various taxes. Consumption taxes tend to bear more heavily on lower-paid cohorts of the population, while income taxes are generally progressive, particularly so in the Irish case, at least in relation to PAYE.

Meanwhile the taxes paid by big corporations are now the subject of international debate and reform talks.

4. What are the policy implications?

The Government commission on welfare and tax, due to be established shortly, will be charged with examining the future Irish tax structure.

Post Covid-19 and with demands on the exchequer rising, it is likely to point to the need to more tax revenue in the years ahead, once the current recession is over. But from where?

The research points to one key area – social security. Here companies are likely to be asked to pay more tax, and quite likely employees too, in return for higher entitlements and also to close the emerging gap in the social security fund.

While a few comparison on entitlements and payments in different countries would be instructive, Covid-19 is certainly put areas like sick pay and supports for short-term work, unemployment, training and so on into the spotlight. And higher PRSI is a clear way to pay this.

However as the researchers point out, PRSI is a gap between what employers pay out and employees take home and are the largest contributor to the non-wage cost of employing people.

What of other possible revenue sources? The left, including Sinn Féin, have called for more tax on higher paid employees and earners. The data does show that taxes on labour are relatively low here, but this is due in part to PRSI.

Two issues raise their head in discussing income taxes. One, should the highest paid be asked to pay a bit more and second should lower paid people, many now not in the net at all, be expected to pay a small amount. Both are politically difficult. For middle earners, meanwhile, most agree that the bill is currently high enough.

With relatively high taxes on consumption, this is one area where the burden is unlikely to rise. However capital and property taxes, where in some cases the burden here is low by international standards, could be looked at.

This is politically difficult too – there has been a successive ducking of any reform of the local property tax, still based on 2011 valuations.

Capital gains tax here is relatively high – and while senior civil servants raise the option each year of increasing the inheritance tax take, one way of taxing wealth, politicians tend to say “no thanks”.

Some kind of general wealth tax could come on the agenda, but reluctance to tax the main source of wealth, the family home, means it is unclear how much those would raise.

The final point is that the ESRI researchers did suggest that current tax policies, including low tax on labour, do probably boost growth here.

So hiking taxes, including PRSI, could have an impact. And in the case of corporate tax, while are effective rate is low, revenues have soared and account for a higher proportion of total revenues here than the international average.

While looking for extra tax, there really are no easy answers.