Remember the national debt? During the financial crisis Ireland’s high debt levels, combined with a sudden hole in the annual budget, threw the State into crisis, eventually leading to the Troika bailout agreed in late 2010. Now, with the exchequer in surplus, the national debt has been largely forgotten. But at €223 billion, it is still lurking and the annual report on the national debt, published this week, points out that per head of population this is one of the highest national debts internationally. So does this matter?

Measuring the debt

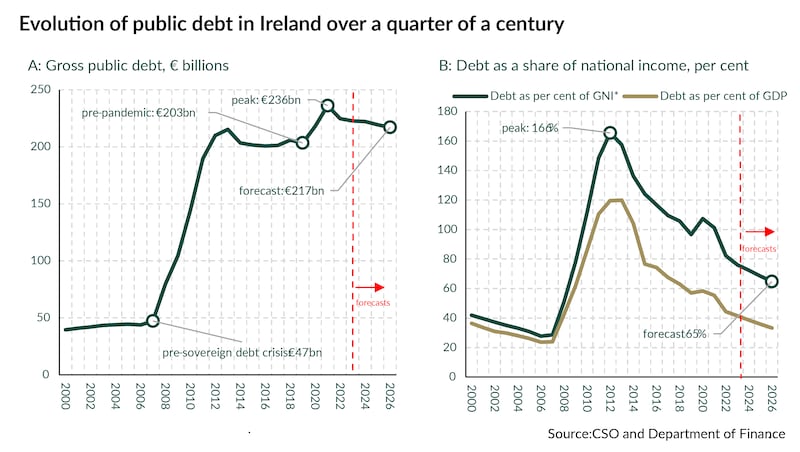

Ireland’s debt exploded during the financial crash, due to the hole which emerged in the public finances as tax revenues collapsed and the cost of bailing out the banks. The debt rose from €47 billion in 2007 to €215 billion by 2013. In cash terms, it fell back to close to €200 billion before the pandemic, but then rose sharply due to the cost of Covid-19 supports to €236 billion in 2021. The subsequent mini-boom in growth and taxes reduced it to around €223 billion by the end of last year.

There are a few metrics which show that, while the cash debt level is high, the dangers have fallen from the dark days of the bailout. Then, the level of the national debt was equivalent to around 160 per cent of GNI* – the aggregate developed by the Central Statistics Office to factor out some of the multinational distortions (it was about 120 per cent of GDP). Now it is around 76 per cent.

Per head of population, the debt was a modest €10,000 in the early 2000s, but its current level of €42,000 it not far off its post-crash peak. While the per head calculations are only indicative (no one is going to come knocking at your door looking for the cash back), we can see how the debt “burden” – its size in relation to the economy – has fallen as growth and inflation have an impact. However, the actual stock of debt as a percentage of annual Government revenue is 178 per cent, high by EU standards.

READ MORE

Lower interest rates – at least until recently – have also helped. A lot. The collapse in borrowing costs as central banks stepped in after the financial crash allowed the State, via the National Treasury Management Agency, to refinance old borrowings at rock-bottom rates. Along with strong growth this ensured the debt ratio has fallen. And the cost of annual repayments were equal to about 3 per cent of Government revenue last year, versus 13 per cent a decade ago. In terms of today’s money, that is an annual saving of around €10 billion.

So why worry?

Fifteen years ago we were all experts on the national debt and on the debts in the banking system. It was mission critical for Ireland. Arguably, the debt is now more like a sleeping giant which we must hope never wakes up. Ireland’s public finances are forecast to remain in surplus, meaning that while cash will need to be raised to pay off maturing debt, there will not be a need, on current forecasts, to borrow more to close a gap between annual government spending and revenue. The contingent liabilities on the national balance sheet from the banking guarantee have more or less gone. As long as nominal economic growth remains higher than the debt interest rate, the dynamics for Ireland will remain positive. Also, while Ireland’s gross national debt is large, net debt, counting in the financial assets on the State’s balance sheet, is lower; these assets amounted to €36.7 billion at the end of 2022, reducing the debt-to-GNI* ratio at that date from 82.3 per cent to 68.9 per cent.

Sudden shock

We saw in 2008 how problems building up over many years can suddenly explode. Ireland fell into the old Hemmingway trap of going broke in two ways – “Gradually, then suddenly”. And the last few years have seen the international economy hit by a number of unforeseen events – the pandemic, the war in Ukraine and now Gaza, threats to shipping and geopolitical tensions. Ireland could, as the department’s report points out, get caught up in some rerun of a euro crisis, even though it now looks relatively well placed by EU standards, or a wider international debt scare. The private sector may have limits to its ability to lend to governments, the report says, while central banks are trying to unwind their holdings of official debt.

[ Will Generation Z be better off than their parents?Opens in new window ]

The report examines a number of shocks which could hit the economy, ranging from a recession to a fall-off in what are estimated to be the windfall elements of corporation tax receipts. To make a judgment on the resilience of the Irish public finances, you need to decide how vulnerable you believe this revenue is; in truth, we do not know. The report points to the risk that such shocks would sent Ireland’s already elevated debt level yet higher, potentially leading to lenders looking for higher interest rates. With significant borrowings due to be refinanced over the coming years – around one third of medium to longer-term debt runs out over the next five years – maintaining the confidence of lenders is important.

The point is not that any of these things are forecast to happen. It is that the high existing level of the national debt does create some vulnerabilities for the years ahead which need to be taken into account in planning policy.

The slow squeeze

Shocks can, by their nature, never be forecast. But longer-term developments can be planned for. Bodies such as the Irish Fiscal Advisory Council have warned for some time of the significant cost of demographic change and decarbonisation. We know there are significant costs coming down the tracks here for Ireland. The department’s report also mentions two other big global factors – digitalisation and potential deglobalisation (the pulling in of supply chains for political reasons), both of which bring threats and opportunities.

[ Corporate tax take likely to evolve from win-win of recent yearsOpens in new window ]

The resulting pressures on expenditure and the potential impact on growth and interest rates could, the department warns, upset the positive outlook for the current short-term dynamics which are acting to reduce the burden of the national debt. In particular, the ageing of the population will slow the growth potential of the economy, reducing tax revenue growth and adding to spending pressures. This slow squeeze on the public finances in the years ahead could make what we are now living through look like something of a golden era.

The policy implications

The message for policymakers is that the national debt remains a constraint on planning. It would be a serious error to bet the farm on a continuation of corporate tax revenues at current levels by using all this money to prop up recurring spending. To try to avoid this, the current Government has put cash aside in a National Reserve Fund and is planning to create two further funds, with obligations on the State to pay in cash each year. One of these, a longer-term investment fund, could, on Department of Finance calculations, build up assets of up to €100 billion by 2035. The plan is also to have a shorter-term fund and to use some cash to continue to pay down debt to some extent. In this scenario the gross level of the national debt would remain high, but assets would build up on the other side of the State balance sheet.

Whether the public finances remain strong enough to allow all these things to happen at once is the question, while also funding planned big increases in Government spending. Unlike other European countries – for example France, Germany and the UK – Ireland is not facing the need to cut back or raise taxes to keep the public finances in order. But as spending levels rise here to meet a higher level of revenue, the sums will, sooner or later, start to tighten.