The extent of the economic collapse due to Covid-19 meant most forecasters were expecting a drop in house prices this year. A massive collapse in consumer spending in the second quarter and the effective shutting down of much of the economy did lead to a fall off in transactions and some softness in prices in spring and summer. But the latest figures show mortgage demand recovering and prices in October generally in line with the same month last year, albeit with some differences across the country and between different types of houses. So can the market hold next year in the wake of the Covid-19 economic fallout?

1. The data

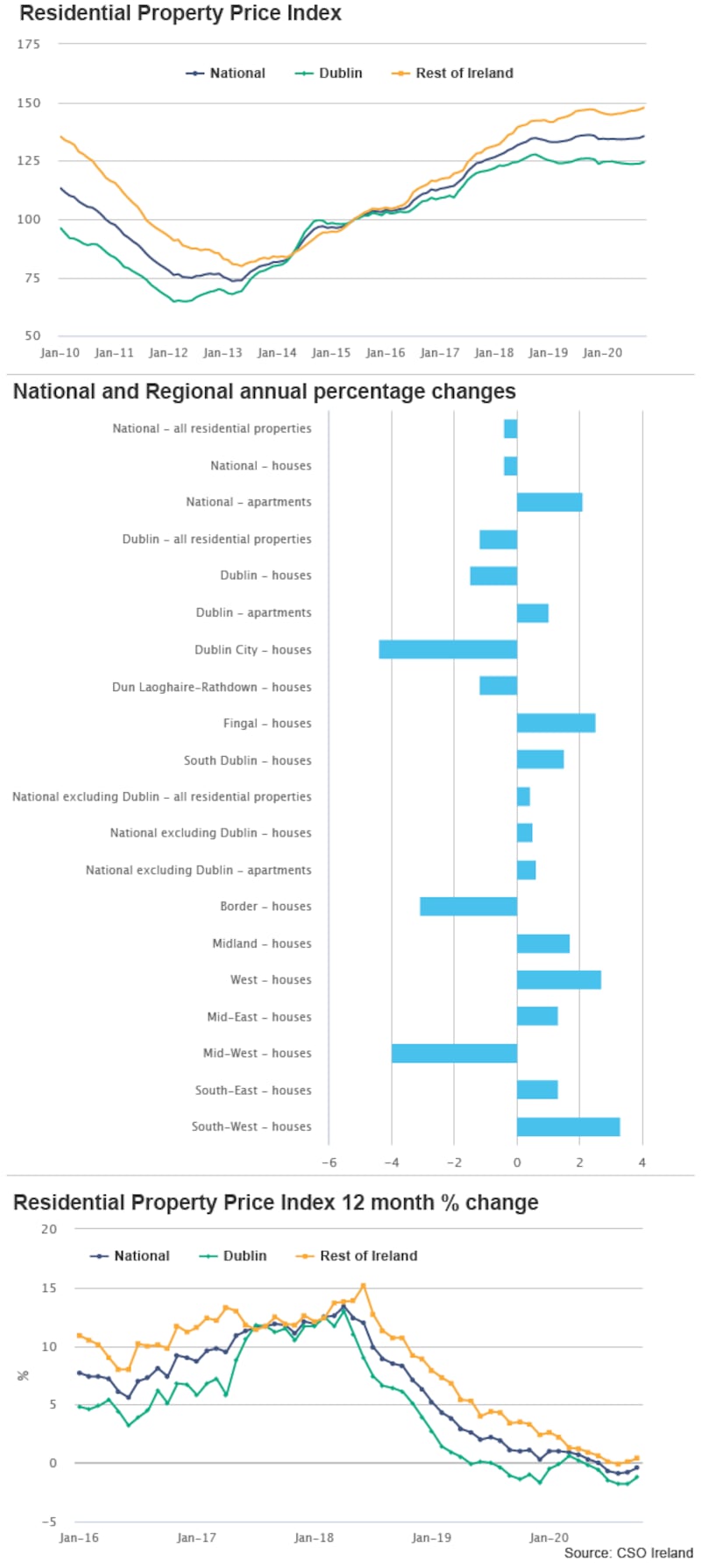

The latest figures from the Central Statistics Office maintain the story of house prices holding up this year. Covid-19 has stopped their upward gallop, but it has not sent them into reverse. Prices in October were up 0.5 per cent on the previous month – the largest monthly rise since July 2019 – and were down just 0.4 per cent on the same month in 2019.

As the graphs show, the pandemic has interrupted the consistent rise in prices of recent years, but hasn’t sent it into reverse. The graph showing the index of prices shows a clear flattening out, while the graph showing the annual percentage change shows that this is now around zero. Whatever the many impacts of the pandemic – slowing transactions initially but also slowing supply – they have more or less balanced out so far in terms of the price impact.

Alongside some recovery in prices, activity in the market has also picked up. “Housing transactions have continued to recover over recent months after sharp falls in the first lockdown in April/May 2020,” notes Goodbody economist Dermot O’Leary. The number of transactions in October was still down 17 per cent on the same month last year, but this is a recovery from earlier months. For the year to date volumes are down 19 per cent.

O’Leary points out that the number of transactions in the new homes market is only down 8 per cent – with activity supported by investment buyers as well as people buying a home to occupy. Second-hand sales are down 22 per cent – many people held off putting homes on the market due to the pandemic.

After falling sharply in the April to June period, mortgage approvals are also picking up, especially for first-time buyers. More than 5,200 new mortgages were approved in October with a value of €1.25 billion, compared to 4,514 with a value of €1.020 billion in the same period last year. For first-time buyers the average approval size of €244,000 was up from €234,000 last year.

2 . The trends

There are not too many major divergences in the trends – though one is evident. Apartment prices are up 2.1 per cent on the year, while house prices are down 0.4 per cent. This probably reflects the ongoing shortage of smaller accommodation – increasingly in demand for smaller households, as well as the continued presence of institutional buyers in the apartment market.

New home prices – including apartments – are up 1.7 per cent in October on a year earlier , while in the second-hand market prices are down 1.6 per cent – not big changes either way, but a trend worth watching.

Regionally, some areas outside Dublin city centre have done better – ranging from the suburbs of Fingal to markets in the South-West. The pandemic may have lessened the demand in Dublin city centre and led to some increase elsewhere as people relocated, though given the low level of transactions it would be a mistake to over-interpret this. While the froth may have gone off the very top of the market, mortgage brokers report continued strong demand for well-located second-hand properties.

In terms of prices, Dun Laoghaire/ Rathdown continues to lead the way nationally, with a (mean) average price of €602,000. The Dublin average is €442,000 while the national average of €294,000. Ireland is not one big property market but a lot of smaller ones, with different prices and characteristics.

Looking at Eircodes, Blackrock in South Dublin, Dublin 4, Dublin 6 and Glenageary all had high average prices, while outside Dublin, Greystones in Co Wicklow was highest.

3. Why have prices held up?

Big economic upheavals usually send house prices lower, but this one has been different, not only in Ireland but internationally. First, the people who have been worst hit are generally younger, less well-off employees in sectors such as accommodation, restaurants, leisure, the arts and retail. Many of these would be renters and would not be earning enough now to consider buying a home – so they weren’t players in the house-buying market. Many of those who were looking to buy are still able to do so as a significant number of sectors continued to operate and earnings were broadly protected. Government schemes, particularly the wage subsidy schemes, kept many in work, earning roughly the same amount as before, and have been vital in supporting activity across the economy. Of course there has been some fallout and some cancelled sales, but the pick-up in mortgage approvals shows demand remains steady. Exactly the same dynamic has been seen in many international markets.

Second, interest rates remain low for borrowers. Rates here have stayed above those elsewhere in the EU, but are still historically low. Together with Government support schemes such as Help-to-Buy, this has helped to support demand.

Finally, supply – already running below any estimate of longer-term demand – has been hit. Construction work stopped for a couple of months earlier in the year – and second-hand supply was also hit as sellers held off. The ESRI estimates that there will be around 18,500 completions this year, down from 21,000 the previous year – and it expects fewer than 20,000 next year as a knock-on from cancelled or delayed starts this year.

All these factors seem to have cancelled out the impact of the general hit to the domestic economy and the uncertainty from the pandemic.

4. And next year?

Relatively low supply will continue to squeeze the market, with the ESRI pointing to a big fall-off in commencements over the spring and summer months. Supply remains well below long-term demand needs, recently estimated by the ESRI at 28,000 per annum.

In terms of demand, a possible lockdown early in 2021 could hit the market. Internationally, forecasters have also wondered whether the fallout from the pandemic – bankruptcies and high unemployment – will hit housing markets in 2021.

However as the ESRI points out in its latest quarterly commentary, the widespread availability of a vaccine will help reduce unemployment and uncertainty and this “may result in significant upward pressure on housing demand in the second half of 2021.”

So while the early part of next year is hard to forecast, restrained supply and strong demand later in the year is surely likely to support prices and lead to rises in at least some parts of the market.

There area two uncertainties to watch. One is Brexit. While a deal between the EU and UK looks on the cards at the time of writing, a no-deal Brexit would cut GDP growth sharply next year – from around 4 to 5 per cent next year to perhaps 1 to 2 per cent on most forecasts. This would hit some sectors hard, keep unemployment high, hit disposable incomes and foster more uncertainty in the housing market and wider economy, at least for a time.

The second factor is what happens when Covid-19 supports start to be wound down. Internationally forecasters have been concerned about the impact of this as bankruptcies and hits to income are likely to follow, at a level hard to forecast. So there could be something of a Covid economic hangover.

5. The longer-term issues

Post Covid-19, there are a few key issues for policymakers. The first is the one which has been obvious for some years – lack of supply, particularly in some parts of the market, including smaller accommodation and social and affordable homes. The Government is also supporting demand via the Help To Buy scheme, offering a tax rebate to first-time buyers and other measures. But will this just push prices higher? A key issue for buyers and the market is the purchase by investment funds – so-called non-households accounted for almost half the sales in the Dublin market so far this year.

Beyond that, Covid-19 has raised some questions about the direction of housing policy. A key focus of national planing is now so-called densification – smaller housing units, closer to city centres, served by public transport. This is seen as the environmentally best way forward. But it is a model built on the idea that many people go to work in the city centre every day. And is this now the future post-Covid for a large cohort who can work from home? Your calculation of where to live might be very different if you go to the workplace, say, two days a week rather than five.