The full impact of the tracker mortgage scandal was laid bare in the Central Bank of Ireland's final report on the issues on Tuesday. It made for depressing reading.

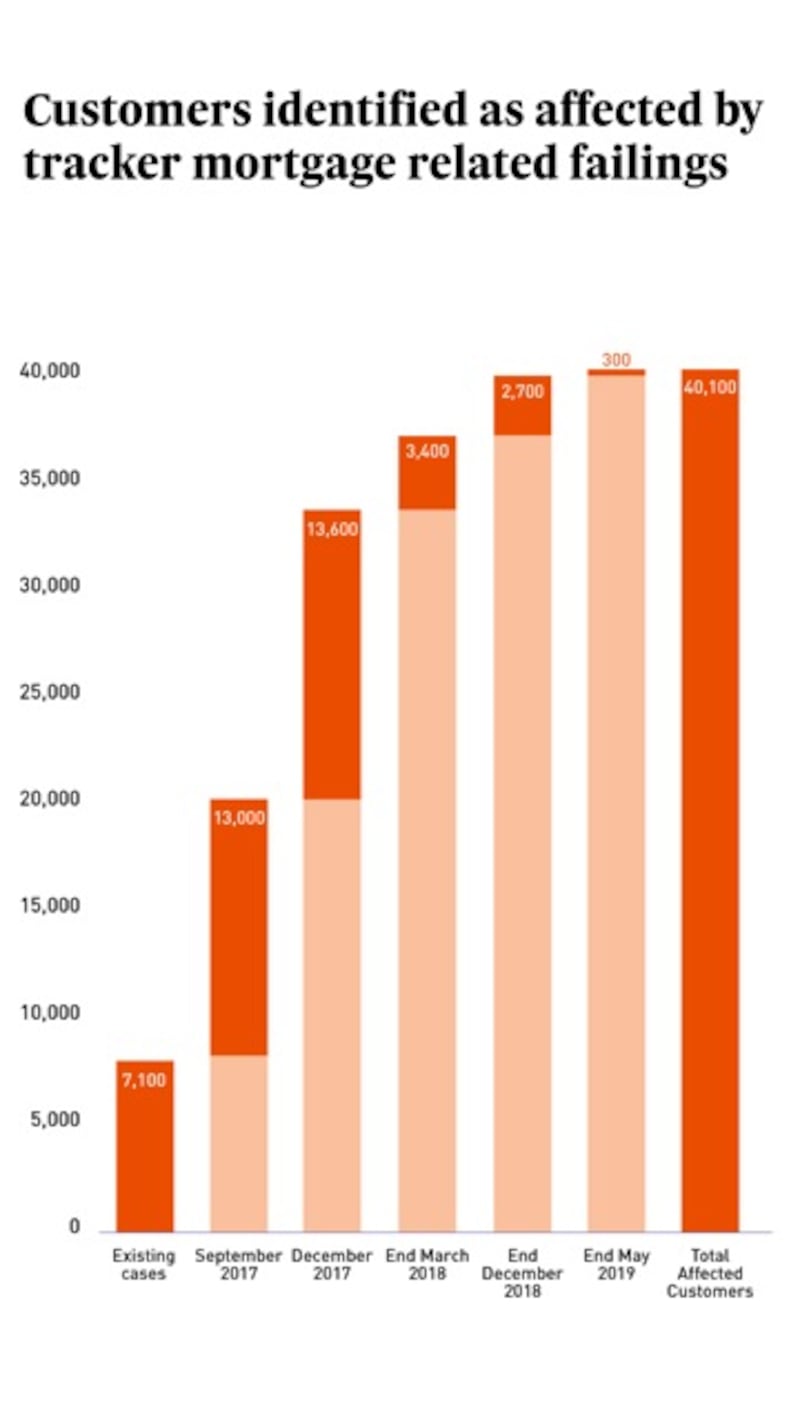

Some 40,100 customer accounts were impacted, with the banks paying out €683 million in financial redress by the end of May, with more to come. A big chunk of that money belonged to Irish taxpayers, given that that the State part-owns AIB, Bank of Ireland and Permanent TSB. We can add that to the €64 billion bailout bill.

Ninety-nine families lost their homes, a devastating outcome for those involved. Another 216 investment properties were lost as part of the scandal.

The average payout for those who lost their family home was €194,000, scant compensation for the stress of losing the roof over your head and the costs of finding a new home. Some relationships probably didn’t survive the strain.

All of this was due to the failure of the various banks post-2008 to offer a low-cost tracker rate to customers who were coming off fixed-rate mortgages, or the fact that the rate offered was higher than it should have been.

In May, Permanent TSB was fined a record €21 million and reprimanded by the Central Bank for its failings. Enforcement action is in train against all of the other lenders. Each will be hit with large penalties.

The Central Bank’s examination has run for more than 3½ years, but this issue has been festering for much longer than that. And the reality is that the banks had to be dragged kicking and screaming to the table before accepting their responsibilities in this sorry saga.

“Notwithstanding the serious issues of customer detriment under consideration in the examination, some lenders initially attempted to minimise the number of affected customers to whom they would have to pay redress and compensation,” the Central Bank report states.

‘Challenged’

The regulator said it “successfully challenged lenders” to include an additional 20,000 customer accounts during the course of its examination, which began in late 2015. That’s almost half the overall total.

In addition, the Central Bank judged the initial redress and compensation offered by the banks to be “materially deficient”. In other words, they were lowballing offers to customers impacted by the tracker issue.

“We reviewed more than 30 iterations and had an estimated 220 engagements with lenders in relation to their proposed redress and compensation schemes, driving substantial improvements in both their schemes and their appeals processes for the benefit of their customers,” the report says.

Derville Rowland, director-general of financial conduct at the Central Bank, said the tracker scandal had caused "immense distress and damage" to customers.

Why did it take until late 2015 for the examination to be launched? And why has it taken 3½ years to get to this point?

“Our message today – to all the firms we regulate – is very clear: where firms fail to protect their customers’ best interests, our response will be robust and the consequences will be serious.”

Strong words, and rightly so, but the Central Bank has questions to answer over this scandal, too. Why did it take until late 2015 for the examination to be launched? And why has it taken 3½ years to get to this point?

We are almost 11 years on from the financial crash, roughly half the lifetime of a typical home loan. It was only after former Central Bank governor Philip Lane was taken to task by the Oireachtas finance committee that the regulator took a big stick to the lenders.

In response to this scandal, the banks have launched the Irish Banking Culture Board, an industry-funded initiative designed to lay the foundations for an "authentic, sustainable cultural change" within the sector. The board is chaired by Mr Justice John Hedigan, a respected former judge, but will have no regulatory powers.

Positive influence

No doubt the board members intend to be a positive influence on the industry over the next few years – but it won’t work. Each bank has its own culture, and every lender is responsible for how they treat they customers. Culture can’t be outsourced to a third-party body, however well-meaning.

In my experience, the banks have been led by decent people over the years and yet they continue to walk themselves into trouble: Dirt tax evasion, ICI, John Rusnak, the bank guarantee, trackers and more besides.

There is clearly something fundamentally wrong with the culture within the industry and the individual banks that such major issues keep cropping up.

On Monday, Brian Hayes, the politician-turned-chief spokesman for the banking industry, had a pop at those who are bank-bashing, in an interview with Sean O'Rourke's RTÉ radio show.

Hiring Hayes as head of the Banking & Payments Federation Ireland was a smart move by the banks. He is articulate, politically savvy, financially literate and well able to debate whatever point he is trying to make.

Rebuilding trust and reputation in Ireland's banking sector is a challenge that the industry fully recognises

But he also runs the risk of being a patsy for an industry that has repeatedly mistreated its customers over many, many years.

In a statement reacting to the Central Bank’s report, Hayes said the tracker mortgage scandal represented a “shameful chapter” in Irish banking history, which caused “great distress and financial damage to many bank customers”.

“Rebuilding trust and reputation in Ireland’s banking sector is a challenge that the industry fully recognises. We are determined to fix the problems.”

Fine words, but it’s long past time for the industry to put them into practice. Not just occasionally but again, and again and again.