[ full series of articles is available hereOpens in new window ]

You're retired and many of those big lifetime financial decisions, such as how much you've managed to save for your pension and how you've invested it, are long made. You're already living on the basis of how well or otherwise those turned out to be. But the next stage of your life, particularly your early 70s, can also be crucial in determining how your later years might play out.

Not only that, but they can only determine what – if anything – you’d like to leave behind to your loved ones.

So what are the mistakes that can be made?

Not getting your house in order

First things first. Suzanne Cashin, head of retirement assets at Tilman Brewin Dolphin, advises that you need to embrace the rules on "rights of survivorship" at this stage of your life, and make sure that bank accounts and investments are in joint names. Otherwise, you risk your partner or loved ones not having access to money in the event of your death.

“You could see one spouse ending up with no access to funds or investments until probate on the will is done, so I encourage people to get their house in order,” she says, adding that couples should also start taking financial meetings jointly.

People also need to consider an enduring power of attorney and a living will, with Cashin noting that having someone in the family who is familiar with the assets can be very helpful if someone becomes mentally incapacitated or dies.

Living wills, which set out your wishes for end-of-life care, can also be enormously helpful to both medical staff and families. “It takes awkward decisions out of the family,” says Cashin.

Unfortunately, the 2015 Assisted Decision-Making (Capacity) Act, which provides the first legal protection for a person’s living will in Ireland, has not yet “commenced”, or been activated, three years after it was signed into law.

Disregarding annuities

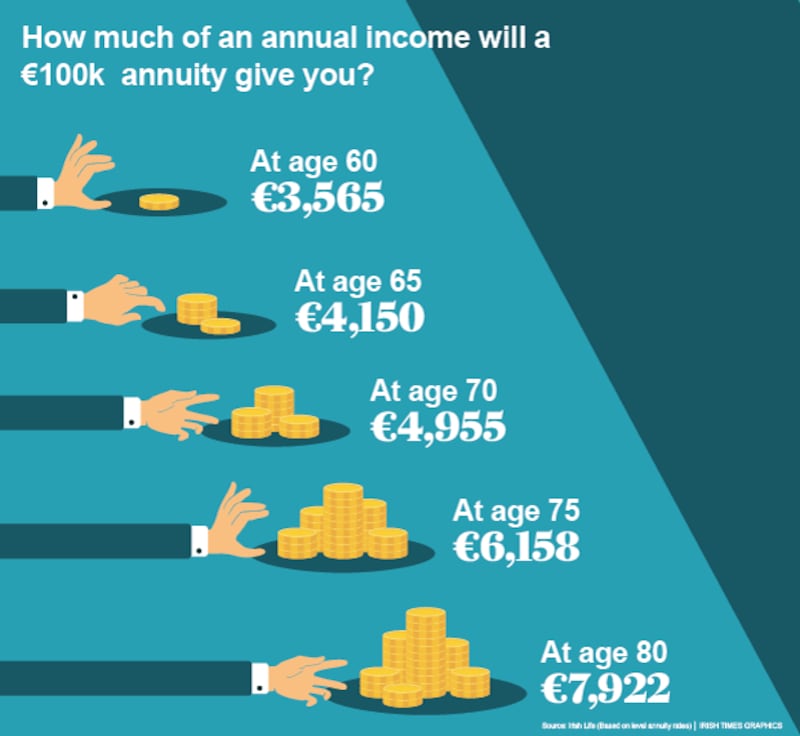

Annuity rates might have been penurious when you first retired and no one is suggesting that they have got any more generous since. But now that you're in your 70s or 80s, the rates might be more appealing. And the peace of mind and certainty offered by an annuity might be just what you need.

As Cashin notes, a man aged 75 can currently get a level annuity rate of about 6 per cent. According to figures from Irish Life, a pension fund of €100,000 would give an annual income of €6,158, based on an annuity rate of 6.2 per cent. This compares with a lower rate of just 4.2 per cent, or an annual income of €4,150, available for someone aged 65.

Of course, that might not seem like a great idea to people who were looking at securing annuity rates of about 6 per cent at age 65 around the turn of the millennium. And even at 6 per cent, you’d want to be living well into your 90s for it to make financial sense, but it does show the relatively better value available as you get older.

For many in their 70s and 80s, downsizing to a new, smaller, warmer property can become a priority

Approved retirement funds (ARFs) can be more attractive in that the value of the fund passes on tax free to a spouse, whereas most annuities die with you. But the guaranteed income can provide peace of mind at a time when you need it most.

As Cashin notes, given a mandatory drawdown level of 5 per cent when you’re aged over 70 on an ARF, and annual fees, you’re looking at returning 6 per cent a year or risking eating into your capital. But this is not easily achieved if you’re unwilling to take on risk.

Thinking downsizing will be easy

For many people in their 70s and 80s, downsizing to a new, smaller, warmer and easier-to-maintain property can become a priority. It can also free up capital to be spent on retirement. But it’s not always easy.

For Paul Murgatroyd, director of research and business development at DNG, it often comes down to a lack of suitable accommodation.

He cites the recent example of an elderly couple looking to downsize to a new apartment development in their locality. But the apartments were snapped up by an investment fund, and the couple never got a chance to purchase.

“They’re certainly removing some choice for buyers in certain localities,” he says of property funds and real-estate investment trusts, adding that one question he has is why there has been so little development of assisted independent living premises along the lines of those we see in the UK.

“I think it’s going to be a growing issue, given the advancing age of the population. Why aren’t these being developed? There must be the demand for them,” he says, adding that such properties could serve as a “halfway house between nursing home care and fully independent living”.

Another factor inhibiting those wishing to trade down is the lack of bridging finance.

“Older people don’t want to have to sell first to get the equity to go and buy again, as they fear they might not find anything,” he says, adding that they are also not keen to leave themselves open to the “vagaries of the rental market” if they don’t succeed in finding a new home to buy.

But if you don’t have the extra funds to do this yourself, it is virtually impossible in the absence of bridging finance.

It’s also important not to underestimate the emotional connection people can have with a family home. “It’s part of their past, it’s their history; they don’t want to give it up and move into the unknown,” says Murgatroyd.

Dismissing estate planning

You may have a little or a lot but, as Marie Bradley, managing partner at Bradley Tax Consulting, points out, estate planning is really for everyone, and not just the wealthy.

“The reason for that is the lower CAT [capital acquisitions tax] threshold between parent and child,” she says.

The threshold has fallen from €528,521 back in 2008 to just €310,000 today (rising to €320,000 from next year following a €10,000 increase in the recent budget).

If you're a regular pensioner, living in Dublin, and by chance or circumstance have a very valuable family home, you mightn't actually realise the value of your estate and thus might not realise the sizeable tax bill you could be leaving behind for your family.

Bradley gives the example of a pensioner with two children and an estate of €1 million. With the parent-to-child threshold now €310,000, this leaves a taxable sum of €380,000.

Based on CAT of 33 per cent, this gives rise to a tax bill of a not-so-insignificant €125,400. “And where’s that money going to come from?” she asks.

Bradley is also keen for people to understand the differences between a transfer of your estate, or assets, in your lifetime, and upon your death. In the event of the former, you’ll have to consider capital gains tax, as well as CAT and stamp duty, although CGT paid can be used to mitigate CAT.

This makes lifetime transfers generally more costly, although as Bradley notes, some children may need a dig-out earlier on.

But of course it’s not a business transaction, and emotions can run high.

“There can be tensions in families. You’ll have the good cops and bad cops,” says Bradley, adding that some will have a view that one child has already got enough, while another may not have.

Determining the wishes of the person/couple leaving the money behind is key.

“What I find is very important is that we meet them on their own,” says Bradley, “as you just don’t know what pent-up tensions there are. It’s a bit like someone drafting a will. You don’t want to have someone in the room”.

And don’t leave it too late

“Sometimes you might need a lead-in time to do tax planning, and if you come in [to plan] in your 80s, there might not be enough time,” says Bradley, adding that she encourages people to review their wills every five years.

“It’s a bit like going to your doctor,” she says.

When you do look at your will, try to maximise thresholds. So, in a family with two children, two in-laws and two grandchildren, for example, Bradley suggests that the two children get €320,000 each; the grandchildren €32,500 each; and the in-laws €16,250 each. This means that almost €740,000 can be transferred without triggering CAT.

Not rebalancing investments

It’s time to get smart when it comes to how you’re invested – and getting your investments to really work for you.

There’s no point investing in a high-risk strategy with a long-term horizon if you may not be around to weather its ups and downs. And you’ll also want to think about tax efficiency. If you’re looking to offset nursing-home costs in the future, for example, by claiming tax relief at the top rate you’ll need to have some income to offset it against.

I'd encourage people to have a big party, celebrate everything, enjoy everything. It's their wealth and it's for them to spend as they choose

As Cashin notes, a portfolio of dividend-paying shares can give you this, as you’ll pay income tax on your dividends. Money in life-wrapped bonds or funds is subject to exit tax, and so no such offset is available.

Of course, as so many people invested in blue-chip bank and other dividend-yielding shares such as Waterford Wedgwood discovered, a dividend today is no guarantee of a dividend tomorrow.

Leaving yourself short

While it’s impossible to determine just how much money you might need in the future, it’s better to overestimate rather than underestimate.

“When you’re that age, you need to keep enough for yourself as you don’t know how long you are going to live,” says Bradley, adding that she encourages people to sit down and do the maths on just how much money they might need.

This might include factoring in the costs of nursing-home care, which, if you have to pay it for yourself as your means are too great to qualify for Fair Deal, can be substantial, at more than €50,000 a year in Dublin. TLC Santry, for example, a private nursing home in north Dublin, costs €1,239 a week, or almost €65,000 a year.

Cashin also urges people to close the “Bomad”, or the bank of mum and dad. “At this stage of life, you get people coming in and something close to a hoarding syndrome kicks in. They are very conscious of leaving an estate, and are also maybe embracing the small-gift threshold of €3,000”.

But while it can be good tax planning, giving away sums of cash to your children and grandchildren each year “could potentially leave yourself exposed to running out of cash”, particularly given our longer life expectancy.

But don’t be too tight either

While you might not fully embrace becoming a Ski (spending the kids’ inheritance), where there is money, try to enjoy it.

“I’d encourage people to have a big party, celebrate everything, enjoy everything. It’s their wealth and it’s for them to spend as they choose,” says Bradley.

There is also a risk if you don’t access certain pension funds. According to Cashin, if you have a PRSA and don’t access it before the age of 75, it will become a vested PRSA, following a change in the 2016 Finance Act.

The change was brought in to avoid people passing on the PRSA completely tax free to the surviving spouse.

“It means that the plan is subject to the imputed distribution system thereafter and the plan provider will take the tax on the deemed withdrawal from their PRSA but not pay the net deemed withdrawal to them,” warns Cashin, adding that you’ll also lose the right to a tax-free lump sum and the choice of buying an annuity or ARF with it.

How long more might you live?

Male (non-smoker)

Current age Life expectancy

70-75 79.4-84.4

75-80 82.0-87.0

80-90 84.6-94.6

Female (non-smoker)

Current age Life expectancy

70-75 82.1-87.1

75-80 84.0-89.0

80-90 85.7-95.7

Source: Irishhealth.com

How much of an annuity can you get?

Age Male Female

60 3.625% 3.625%

65 4.210% 4.210%

70 5.015% 5.015%

75 6.218% 6.218%

80 7.982% 7.982%

Source: Irish Life (single life)