The slum of Korogocho lies on the outskirts of Nairobi, the capital of Kenya. More than 260,000 people live here, in shacks made of wood and corrugated steel, crammed between dusty paths and open sewers. Nearby is the huge Dandora dump. In the dead heat the smell of rubbish is overpowering.

Deeper into the slum two men wash a canary-yellow car, music blaring from its radio. A group of children play skittles, using a shoe as the ball and batteries as the skittles. Women cook over open fires. Each step takes us deeper into another era.

Inside one shack, mud walls and a spartan room are visible through the gloom. A tiny, sparrow-like woman sits passively. She wears a pink fleece and a yellow headscarf. Two children sit silently in a corner. When she speaks her voice is so quiet it is hard to hear.

Naomi Wanjiru Nganga is 34 and weakened by pneumonia. She has four children, aged from four to 16. Unable to work, she collects and sells cardboard boxes and sometimes washes clothes. In a good week she earns 600 Kenyan shillings – about €5, not enough for her or her children to survive. Nganga lives in extreme poverty. Yet when she speaks her overriding sentiment is hope in humanity and in the future. The world she sees is a good place.

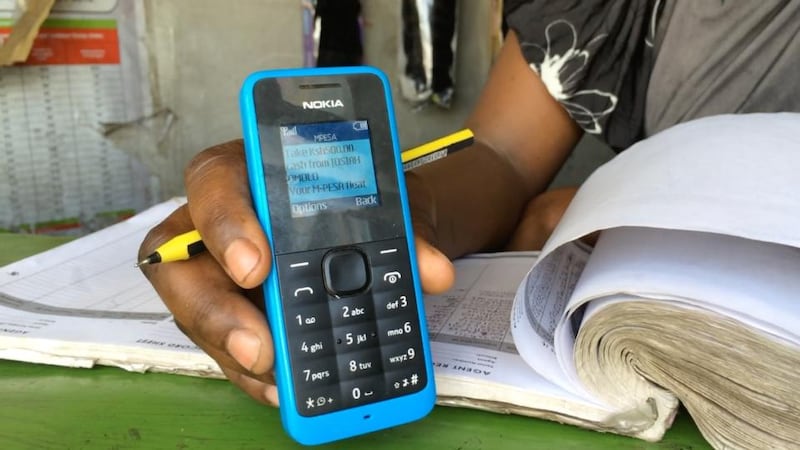

From a drawer she produces a basic mobile phone. It is the first 21st-century object we have seen in the slum. But this basic technology has transformed Nganga’s life. It has also transformed Kenya, and in time it will do the same for many developing countries.

She uses the phone for M-Pesa, or mobile money. (Pesa is Swahili for money.) Every day she and millions of other Kenyans transfer money by mobile phone as easily as they send text messages.

Kenya leads the world in M-Pesa. A decade ago the gap between the developing and developed worlds was widening. Sub-Saharan Africa had few landlines and little broadband. Most people had no access to banks; economies relied on cash.

Initially, mobile phones looked as if they would be as inaccessible to poor Africans as other technology had been. In 2002 Kenya had just two mobile phones for every 100 of its 38 million people. Ireland had 77 per 100. In Kenya that picture changed quickly.

Multinationals arrive

Multinational telecom companies arrived and, with few planning restrictions, quickly erected mobile-phone masts, even in remote areas. Cheap handsets – often second hand, always basic – became available. Although the prepaid service that most subscribers used were costly for ordinary Kenyans, they enabled contact with villages half a day away, unreachable by road, and without water or electricity. This transformed both business and social and family life.

Between 2002 and 2006 the number of mobile phones in Kenya increased from one million to 10 million.

Just as mobiles had disrupted the conventional landline business, M-Pesa would now disrupt banking. Few Kenyans have bank accounts; even fewer have credit cards. Transferring money was also a problem. Many city workers have moved from rural areas hundreds of kilometres away. The only way they could send money home was by matatu, or minibus taxi, which was inconvenient, time consuming and open to theft.

M-Pesa started off as a social initiative within Safaricom, Kenya's biggest mobile-phone company. In 2003 Nick Hughes of Vodafone, which owned 40 per cent of the company, began a project to explore how mobile phones could help deliver microfinance loans. Some people were already using their phones to move money informally, transferring mobile-phone credit, which could be cashed in, by text. Now software was written to set up a proper money-transfer system that could be used on the simplest phone. It meant money could now be transferred by text message; the recipient could then use a Pin and identification to collect the cash from an agent.

Money real quick

Dr Tonny Omwansa, who teaches computing and informatics at the University of Nairobi, has cowritten a book about M-Pesa, Money Real Quick. We meet in an innovation lab at the campus, on the outskirts of the city, to talk about the growth of mobile money.

Hughes and his colleagues piloted the system in 2005, partly in the slum of Mathare, Omwansa says. They set up agents and gave out mobile phones. Although the system was designed to handle microfinance loans, “they were surprised at how people used it.” Businesses used it to pay other business, or as an overnight safe; and people used it to send money to relatives and to people outside the pilot areas.

Hughes and his colleagues realised the system could have a much wider application than they had envisaged. Safaricom’s chief executive at the time, Michael Joseph, also saw its potential. “I decided this was going to get big,” he told Onwansa. “If people have M-Pesa they will not leave Safaricom. Did I know it was going to be so big? No, I didn’t dream it. None of us did.”

It took off at a gallop. People trusted the mobile companies more than they did the banks and post offices. M-Pesa’s simple slogan, Send Money by Phone, resonated with the Kenyan custom of sending funds home to family.

The service launched in late 2007. People lodged money to their M-Pesa accounts and were charged a small commission when they transferred or received money. Within a few years the service had become ubiquitous, with 30,000 agents. By 2015 almost 18 million Kenyans had accounts; they used it to pay for education, medicine and transport, including matatus, and they used it so much that the system handled 20 per cent of Kenyan GDP.

Today in Korogocho M-Pesa’s green and red logo is everywhere. The system is “less a channel for emoney, more of a new storage channel for distributing cash outside the banking system”, says Omwansa.

Fifty kilometres or so north of Nairobi, in the Rift Valley, is the village of Maai Mahiu, which is little more than a truck stop on the highway to Uganda. A roadside shack houses the Smart Lady Boutique, which displays modern and traditional African dresses.

Its owner, Christine, pops to the M-Pesa agent next door to order clothes from Nairobi. She gives him cash and the details of her M-Pesa account. He lodges the money to her phone, and she then texts it to the wholesaler. Her order will be dispatched within hours.

“I used to have to get a matatu into Nairobi to order clothes,” Christine says. “It took a full day each time, and I had to close the shop. I used to carry the money with me. Now I order and they send the clothes to me.”

At Safaricom’s headquarters in Nairobi Sitoyo Lopokoiyit, the company’s head of strategy in financial services, says that the system’s biggest competitor is cash. In response M-Pesa plans to be available in every conceivable situation, he says, including at supermarkets and airlines.

The concept has been tried in about 20 other countries, including South Africa, Pakistan, Romania and Albania, with varying success. In none of them did M-Pesa become as popular or widespread as it is in Kenya.

Mobile aid

A few months after M-Pesa was launched Kenya plunged into violence over a contested general election; 1,500 people died, and hundreds of thousands of people are estimated to have been displaced, particularly in the Rift Valley north of Nairobi, according to Human Rights Watch.

Anne O’Mahony, Concern’s country director in Kenya at the time, describes the crisis. “There was a complex mix of needs. We could not go out and buy anything and could not distribute plastic sheeting and corrugated metal for shelter. The most practical way of helping was to give money directly. But how could we distribute cash directly in a safe and secure way?”

Concern spoke to Michael Joseph at Safaricom, who agreed to a mobile-phone deal in return for access to the new users. When Concern evaluated the new system it found that M-Pesa transfers were more efficient than distributing food and goods itself, as they had none of the attendant purchase and distribution costs, no middlemen to take a fee, and no goods to go missing. And, as O’Mahoney puts it, “Poor people struggling to survive are in the best position to monitor their own spending.”

The scheme expanded. Families at risk of extreme poverty, usually in Nairobi’s slums, received a monthly transfer for eight or nine months. The monthly sum was modest – 2,000 Kenyan shillings, or about €17.50 – but “a cash transfer is better than a food transfer,” says Wendy Erasmus, O’Mahoney’s successor. “It gives people an independence and a power of decisionmaking. We saw a surprising increase in the number of meals people ate during the day as a result of this small cash transfer. The second thing we saw was that people were able to keep their kids in school or put them back in.”

Some women put money aside to set up small businesses, making bread or chicken soup to sell on the roadside. And when people spend the money at local shops it means that those funds stay in the community. “Cash empowers people,” says Erasmus. “When targeted properly it gives people the choice of doing something that makes their life more sustainable and lifts them out of extreme poverty.”

Back in Korogocho

Back in Korogocho we meet Naomi Wanjiru Nganga again. Hers is one of 407 households taking part in an eight-month cash-transfer scheme. Clearly affected by her illness, she walks slowly to a nearby M-Pesa agent, as she has received a text with her monthly transfer. Nganga shows her phone to the young woman at a counter behind a protective grille, enters her code and shows her ID. Moments later the agent hands over her cash.

What does she do with her 2,000 shillings? “My first priority is school fees for my children, and then food and then my medicine,” she says. “The first thing I do is sit down with my children, and we give a blessing to God and say a prayer of thanks to those who have given the money to us.”

Mobile phones and the epayments they have facilitated are powerful enough to have changed life for millions of Kenyans. But the strong hope for a better future expressed by a sick woman in a desperately poor slum is very powerful, too.

Smart solution: how an Irish charity identifies urban emergencies

Concern’s operation in Korogocho works hard to identify vulnerable children and adults.

The slum has double the national HIV and Aids rate, and high mortality rates mean that many children end up heading households before they are teens. The risk of drifting into drug peddling, prostitution and crime is high.

Here too another innovative use of mobile phones has had a significant effect. Jay Chaudhuri has co-ordinated a new mobile-phone tool to help identify urban emergencies quickly.

“Traditionally in rural areas, rough and low rainfall triggered an emergency where malnutrition rates increased. In urban areas there are usually multiple causes and different contexts.”

The indicators might include families on the edge pulling their children out of school, family debt, access to water, rising food prices, or urban displacement, where families lose their homes.

Concern uses smartphones to do regular surveys of households, gathering data for analysis. “Very quickly we are able to assess if a situation in a certain area is getting worse. Being able to use smartphones is rapidly increasing turnaround time and response,” says Chaudhuri.

Birth of a health project: how mobile phones help reduce infant mortality

The charity World Vision also uses smartphones for a women’s-health project that should reduce infant mortality in rural Kenya. The country has an overall rate of 52 infant deaths per 1,000 live births, but that rises to 126 per 1,000 in some coastal regions.

Cynthia Nyakwama says that in rural areas little information is available to expectant mothers. The local health workers involved in the pilot project are given smartphones to record all the details of a pregnancy and of the pregnant woman’s health.

As well as providing more accurate information about infant mortality, the project involves detailed questionnaires that, when sent back for analysis, can help identify what pregnancies are high risk.

Expectant mothers are sent text messages during their pregnancy, reminding them of appointments or giving advice. Sometimes the information will be sent via the health worker. “For example, we will teach the mother what to do if she starts bleeding in pregnancy,” says Nyakwama.

Her colleague Miriam Mbembe says: “Message development is a continuous process. Breastfeeding is one of the key messages we have been pushing to these women, telling them breast is best for at least six months.”

This article was supported by the Simon Cumbers Media Fund