To decide what might happen to house prices next year we need first to try to work out whether prices are overvalued at the moment – and then look at what factors will affect the outlook into 2023. Neither is straightforward. So what do the economics say?

Are house prices currently too high?

Working out whether housing prices are overvalued is not a simple exercise – economists typically use a range of tools, such as comparing house prices to rents, to income levels and to a range of supply and demand factors.

The result depends a lot on the assumptions you make about the key determinants of house prices and how they interact. And remember that this is not a value judgment based on what level we believe prices should be, it is an attempt to see how they relate to current economic fundamentals.

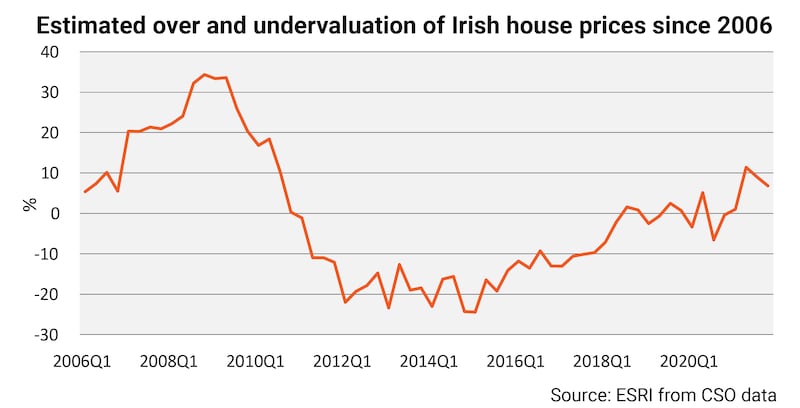

The latest Economic and Social Research Institute (ESRI) quarterly commentary estimates that by early this year Irish house prices were overvalued by around 7 per cent – ESRI research professor Kieran McQuinn says that this overvaluation could now be around 10 per cent.

READ MORE

His analysis is based on modelling which goes back many years and looks at the relationship of house prices to fundamental demographic and economic variables – including population trends, particularly in key house buying ages, housing supply, interest rates and incomes.

This is used to calculate how far prices diverge from their value based on economic fundamentals – either above or below.

This shows that house prices were hugely overvalued before the financial crash- by more than 30 per cent at peak – driven by a credit-fuelled boom, and then collapsed rapidly. European Commission research confirms that the fall here happened much more quickly than elsewhere in the EU, with prices in the Baltic States also falling quickly.

Crucially, interest rates are on the rise – and while only a portion of this has fed through to the new buyers’ market, the rest of the increases will also in time be passed on.

Within a couple of years house prices collapsed to a point where they were undervalued by more than 20 per cent, using the ESRI model. In historical, or international, terms, these were huge swings.

After a few years of stagnation, Irish prices the recovered rapidly, reaching – on the ESRI analysis – a fair value in relation to underlying economic factors by 2018/2019. Noticeably, house price growth had moderated sharply heading into the pandemic. It seemed the market might be moving to some kind of balance.

However, then Covid hit. House prices accelerated thereafter, according to the ESRI research, published in its latest quarterly bulletin, because Covid shutdowns hit supply while a portion of the huge household savings built up during Covid-19 seems to have been diverted back into the housing market, a phenomenon also noted in a number of other international markets. The presence of international investors may also have been a factor supporting prices, McQuinn says.

[ David McWilliams: The financial tide is going out ... Keep your togs onOpens in new window ]

While the ESRI methodology estimates that Irish house prices are now overvalued, not everyone agrees. In its recent Alerts 2023 report, which tries to spot building problems, the European Commission says that its calculations do not see the Irish housing market as being overvalued – it directs its warnings on this score elsewhere.

However, the EU does note in the latest report on Ireland the increased concerns about house prices. And on one factor, affordability, Ireland does score badly, with commission calculations finding it takes 16 years of average income in Ireland to buy a 100sq m apartment, one of the highest of the EU countries measured. How this squares with its assessment that house prices here are not fundamentally overvalued is not clear.

What will the easing of bankers’ pay restrictions do for competition dynamics?

So, what happens next for house prices?

There are a significant number of negatives for prices over the next year. Crucially, interest rates are on the rise – and while only a portion of this has fed through to the new buyers’ market, the rest of the increases will also in time be passed on. And there are clear signals of more to come.

Also, household finances are being squeezed by the cost-of-living crisis, the economy is slowing and confidence is on the wane – all factors which will affect housing demand.

McQuinn says that house prices can be expected to fall back to fundamental value in time, either through a period of stagnation or a shorter-term fall. However, he sees factors that will provide some support for the market in 2023, including signs that, after a rise this year, housing completions in 2023 could stall or even decline.

Rising building starts are slowing housing starts and inward investment. How long the build-up of savings during Covid will affect prices is also unclear. McQuinn says that this is not included in his formal model as a factor as savings levels will have to return to normal sooner or later.

[ Ireland’s rental market is broken – and could be heading for even deeper troubleOpens in new window ]

But for 2023 the deployment of excess savings could again be a factor. Many better-off households still have significant savings, with a record €150 billion sitting in Irish savings accounts in November.

McQuinn says the outlook for house prices next year is hard to call, but he expects a significant slowing in price growth from current levels, though an actual fall in prices may be avoided. However, there are some fundamental factors here relating to demand which will put a floor under prices, he believes.

Longer-term supports to demand

While housing supply remains constrained, the longer-term demand level is driven by population trends. McQuinn says that while previous estimates were that Ireland needed between 30,000 and 35,000 new dwellings annually, the latest census figures, showing a larger population than expected, suggests that this figure probably needs to rise to at least 40,000.

There is also a large latent demand in households, with many younger people forced to continue to live at home due to high rental and house prices – and many renters unable to save for a home due to high rent levels.

House prices look unlikely to head south in the short term, but price growth is already slowing.

In Ireland just 64 per cent of 20-49 year-olds in work have their own place to live, compared to an EU average of 74 per cent. Nor is this generational disadvantaging of younger people in housing unique to Ireland, with OECD data showing that the level of property prices today in the industrialised world are much higher in relation to incomes than for previous generations.

[ Which Irish mortgage borrowers are most exposed as interest rates rise?Opens in new window ]

A question for the Government now, in the current strange economic circumstances, is whether housing demand could remain relatively strong, despite the economic slowdown. So far unemployment has remained very low – just 4.4 per cent on the latest readings – and while problems in the tech sector may affect pockets of the market, it may not have a wider impact.

The unknown factor in the market now is confidence and the impact of the cost-of-living squeeze. This is likely to make buyers more cautious, though the autumn selling season appeared healthy, with the number of transactions in September up 6 per cent on the same month last year at 4,583.

House prices look unlikely to head south in the short term, but price growth is already slowing – from an annual rate of 14 per cent in June to 10.8 per cent in September. The monthly rate of increase also seems to be slowing and, as in the UK, we may see some monthly falls in house prices, even if the annual increases remain in positive territory.