Research by the Central Bank of Ireland shows that more than one in five could save thousands by switching their current mortgage provider. Not everyone can switch, but it's worth taking a look to see if you are eligible.

Just like applying for a mortgage, the process involved in switching isn't an easy one, but the savings you could make by switching mortgage may be worth it.

What's involved in switching?

Step 1: Visit the Competition and Consumer Protection Commission's website to see if you are eligible to switch mortgage.

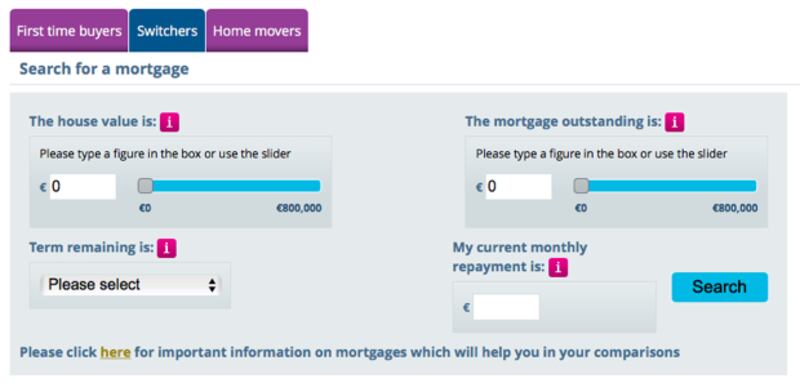

Step 2: Use the handy mortgage comparison tool to compare rates and see how much you could save over the course of your mortgage.

Step 3: Input your mortgage details, including the current value of your home, the outstanding amount you owe, how many years are left on your mortgage and the amount that you pay every month. The mortgage comparison tool will show all of the available options on the market right now, for both fixed-rate and variable-rate mortgages.

Step 4: The mortgage comparison tool will show the difference between what you're paying now and what you could be paying by switching to another provider.

Step 5: If it looks like there's a better deal out there for you and you have made the decision to switch, talk to your lender to see if they'll give you a better rate. You can contact individual lenders or go to the switching section on the bank or mortgage provider's website.

Beware of cash offers and incentives. Incentives can look really attractive but when people compare the value of those incentives to the potential difference in the overall cost over the lifetime of the mortgage, it doesn’t always add up to the best value. Don’t be enticed by freebies like cash back or free legal expenses without looking at the cost of the mortgage over the entire term.

Case study: spotting value when switching provider

John and Mary have an outstanding mortgage of €300,000 on their home, which is currently valued at €360,000. They want to switch mortgage and decide to go with the flexibility of a variable-rate mortgage. Their current loan-to-value ratio is 83 per cent and they have a 25-year term remaining on their mortgage.

Loan-to-value is a percentage representing the amount owing on a mortgage relative to the market value of the property. You have a loan-to-value of 50 per cent if your home is worth €500,000 and you owe €250,000.

John and Mary are instantly drawn to the lender who is offering cash back to the value of 2 per cent of the amount borrowed, and they quickly disregard another lender who has no special offers available.

They are delighted they will be receiving €6,000 cash back to move to Lender A. John and Mary don’t take the time to consider the interest rate with each provider. Lender A, with a loan-to-value greater than 80 per cent, gives John and Mary an APRC of 4.6 per cent, while Lender B gives an APRC of 3.6 per cent for the same loan-to-value ratio.

Over the lifetime of the mortgage with Lender A the cost of credit is approximately €200,249 - the cost of credit shows you the real cost of borrowing. It is the difference between the amount you borrow and the total you will repay including the interest by the end of the loan period. When you deduct the €6,000 cash back John and Mary received, when they drew down their mortgage, the final cost of credit is €194,249. In contrast, the total cost of credit with Lender B is approximately €150,561.

This will prove quite a costly decision for John and Mary. The temptation to take the 2 per cent cash back will ultimately cost them €43,688 over the entire term of the mortgage. Their mortgage repayments with Lender A are €165.63 more expensive a month than they would be with Lender B. Over a year that works out at €1,987, and within three years it amounts to €5,962, meaning that if rates don’t change the benefits of the special offer would have almost disappeared after three years, leaving John and Mary paying €165 more every month on their mortgage for the remaining 22 years.