Why has the European Central Bank increased interest rates over the past year?

Higher interest rates are the European Central Bank’s primary weapon to try to bring down the rate of inflation, which has picked up as economies came out of Covid-19 shutdowns – and then surged due to higher energy prices after the war started in Ukraine.

How do higher interest rates bring down inflation?

They do this by taking money out of people’s pockets – because they are repaying more on borrowings – and thus, bringing down consumer spending. Higher borrowing costs also slow business investment. And so, demand in the economy falls, there is less money around and inflation eases back.

[ Cliff Taylor: Will the new housing plan work and will it lower prices?Opens in new window ]

But inflation this time around was set off by higher energy prices, not consumers spending more?

True. And this was one reason why central banks across the world, particularly the ECB, were slow to react when energy prices rose initially and prices in some other areas were increased due to supply chain problems after Covid-19.

These were problems in the supply side of the economy, not due to higher demand. And higher interest rates do little to directly target them. The trouble since then is that inflation has spread across economies and is evident in the prices of a whole range of goods and services.

READ MORE

Just look at food prices, for example, and the big increases in the price of many services, notably air travel. Signs that inflation is getting embedded in this way – and may, in turn, be leading to higher wage demands – are a red flag for central banks.

So, they just keep on hiking interest rates no matter what problems it causes for households?

Yes. The ECB’s target is to keep inflation at around 2 per cent and with headline inflation in the euro area at 6.9 per cent, this still looks a long way off.

Even stripping out inflation from energy and food, seen as the most volatile sectors, so-called core inflation is still increasing at an annual rate of 5.7 per cent.

But ECB interest rates have already gone up by 3.5 percentage points since last July. Surely that is making a difference?

It is. But the full impact of higher interest rates takes time to feed through. It is a while before banks pass on the increases to customers and more time passes before they react.

These time lags can be unpredictable and the extent of the impact can be uncertain. Central banks like the ECB are obsessively watching price data and surveying consumers on their expectations but there is no exact formula here – a lot of it is down to judgment.

So far, the ECB judges that higher rates are starting to have an impact but that there is more work to do.

Why do some shareholders in the Republic's largest private residential landlord feel shortchanged?

So, more is to come?

Yes, but how much is hard to know and there are clearly different views on the ECB board, as are now being expressed publicly. Another increase is expected next week – there will be intense interest in whether it is a quarter point rise or another half point increase.

Markets expect a further increase or two beyond that. At the moment, they anticipate that the ECB deposit rate, now 3 per cent, will top out somewhere around 3.75 per cent.

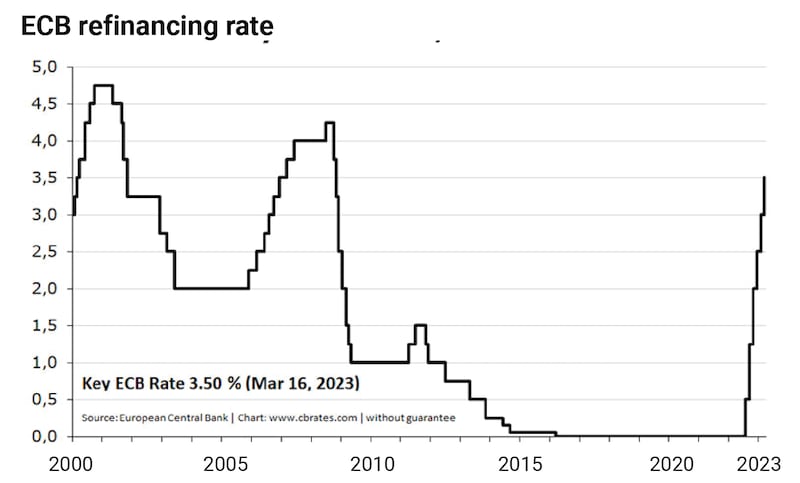

So, that could be three more quarter point rises at the next three meetings. Uncertainty remains around these forecasts, however. (Note, too, that another key ECB interest rate – the refinancing rate – is now at 3.5 per cent and this is the rate off which Irish tracker mortgages are priced.)

New Central Bank of Ireland research estimates that around 20 per cent of borrowers – many of them tracker mortgage holders who took out loans before the financial crash – are most exposed, facing increases in monthly repayments of up to 50 per cent compared to the position last July before rate increases started.

Some 40 per cent of borrowers, including many who have recently taken out mortgages, are protected by being on fixed rates, though these will gradually run out in the years ahead. The average monthly repayment increase is 13 to 16 per cent, depending on how far rates rise.

Is there a risk of the cure here being worse than the disease?

The ECB’s determination to bring down inflation is based on the idea that the cost of getting inflation down now is worth paying to avert the longer-term price of high inflation – and the outside risk of some kind of hyper inflation.

The bank has been a bit higher before but what is happening is some change from the rock bottom rates which have applied over the past decade and the pace of increase has been the most rapid in the ECB’s history.

It is trying to balance two risks. One is that it does too much and drives euro zone economies into recession unnecessarily; the other is that it does not do enough and lets inflation rip. The unprecedented nature of what we have seen over the past couple of years means there is no clear answer.

[ Irish mortgage rates fell surprisingly in FebruaryOpens in new window ]

But, isn’t a lot of inflation now due to firms profiteering?

There is certainly evidence that some firms at least have been cashing in on the big jump in demand – so-called greedflation.

United States evidence showed profit margins at levels not seen since the second World War and in the European Union, too. Profits are on the up, the ECB believes.

Christine Lagarde, the central bank’s president, has warned of the risks of a tit-for-tat process where companies increase prices – and profits – and their employees look for higher wages, with a potentially dangerous cycle developing.

Companies risk losing market share if they keep increasing prices in advance of everyone else, however, so it may be that profiteering starts to ease off after a period. It should do if markets operate properly.

Why can’t governments do something about this?

It is difficult. Governments can give out to businesses and this may have an impact. Most markets either operate freely or – in the case of things like energy – are subject to a set of regulatory rules which have been build up to engender competition.

There have certainly been problems in energy markets, where the way they are structured helped to keep prices high last year and declines have been slow to pass on to consumers. Irish energy providers plead that they are not profiteering – and had to buy energy in advance at high prices to guarantee supply.

Trends elsewhere in Europe and the fall in wholesale prices now has them under pressure to move, however. Customers may start to see some declines before too long. Unless they tear up the rule book, Government cannot force this to happen.

In terms of energy, what EU governments are doing is imposing taxes to grab the additional profit being made by some electricity generators and redistributing it to the public via measures such as the electricity credit and special welfare payments.

Nor can governments realistically step in to control the price of, say, food. Competition in the market – the fight for market share – is meant to do this and price controls are a policy not generally used in modern market economies. Instead, governments try to ensure that markets operate in a properly competitive way.

Governments could, of course, also act to withdraw money from economies by cutting spending or hiking taxes as another way to control inflation. In Europe, the ECB has been telling them to quickly phase out temporary energy supports. The main running in fighting inflation will remain with the ECB.

So, the punter gets caught with higher prices and higher interest rates?

Yes. That is what it looks like at the moment. Unfortunately, the rise in interest rates does not seem to be over.

And while inflation is easing, it remains stubbornly high. Tensions between governments and the ECB may well build as the summer goes on, particularly if economic growth slows. But, having given the ECB the mandate to control inflation – and made it independent – there is only so much governments can do.