Last week in this newspaper, economist David McWilliams wrote that Irish banks are “taking the mick” when it comes to passing on the benefit of interest rate hikes, citing S&P Global Ratings figures showing that Irish banks have passed on to Irish savers just 7 per cent of the recent ECB rate rises, as opposed to the 43 per cent of Bank of England increases that have been passed on by British banks.

Minister for Higher Education Simon Harris separately said that it was “offensive” for Irish banks to be “complete and utter laggards” when it comes to passing on rates.

It is quite clear that, despite the rise in European interest rates over the past year – to 4.25 per cent as of the end of July, with a further hike potentially on the cards in September – returns available for Irish savers have not moved in parallel.

Banks are still paying as little as 0 per cent on instant access accounts (Bank of Ireland), while the best fixed-term products are offering about 2 per cent a year – and you have to lock away your money for at least 18 months to get this.

READ MORE

While the banking industry and others have argued that banks have, in similar vein, not imposed the full whack of ECB rate hikes on mortgage customers, this too has changed in recent months. Latest Central Bank figures show that average new mortgage rates in Ireland now exceed the euro zone average – at 4.04 per cent, compared with 3.79 per cent in Europe: just a few months ago, they were below the average across the bloc. There is no doubt that Irish savers are being poorly treated compared with European and UK norms.

With both savings rates, and a preference for deposits, remaining strong, there appears to be little incentive to offer a better rate

Given such poor returns, one might expect savings providers to be punished by consumers leaving only low levels of savings on deposit. However, this hasn’t been the case in Ireland. Yes, the amount people are saving continues to fall as we move further away form the era of Covid lockdowns – the household savings rate fell to 14 per cent in the first three months of the year from 24 per cent at the end of 2022, according to Central Statistics Office figures. However, as the CSO notes, this rate of saving is similar to pre-pandemic levels. Part of the reason it has been falling is down to reduced levels of disposable incomes on the back of the hike in the cost of living.

Moreover, the CSO notes, “most of this saving went into bank deposits and to buying or improving homes”.

That savings rate is on a par with levels across Europe: most recent figures from Eurostat point to a household savings rate of 14 per cent in the euro zone in the first quarter of 2023, and a rate of 13.3 per cent across the EU.

But with both savings rates, and a preference for deposits, remaining strong, there appears to be little incentive to offer a better rate.

State savings

Unless of course, the National Treasury Management Agency (NTMA) moved to hike the rates it offers to savers. This Government agency could shake up the market dramatically by putting the rates it offers on State savings on a par with European norms – yet it hasn’t.

So it’s not just the banks that are failing Irish savers; the State is too through its State savings operation, which is delivered via An Post and offers a range of short and long-term savings products, as well as prize bonds.

While much of the recent rhetoric has been aimed at getting the Government to be more active in engaging with banks as a means to increase rates, increasing competition via the State savings offering is another route. After all, returns here are also well out of whack with the current interest-rate environment.

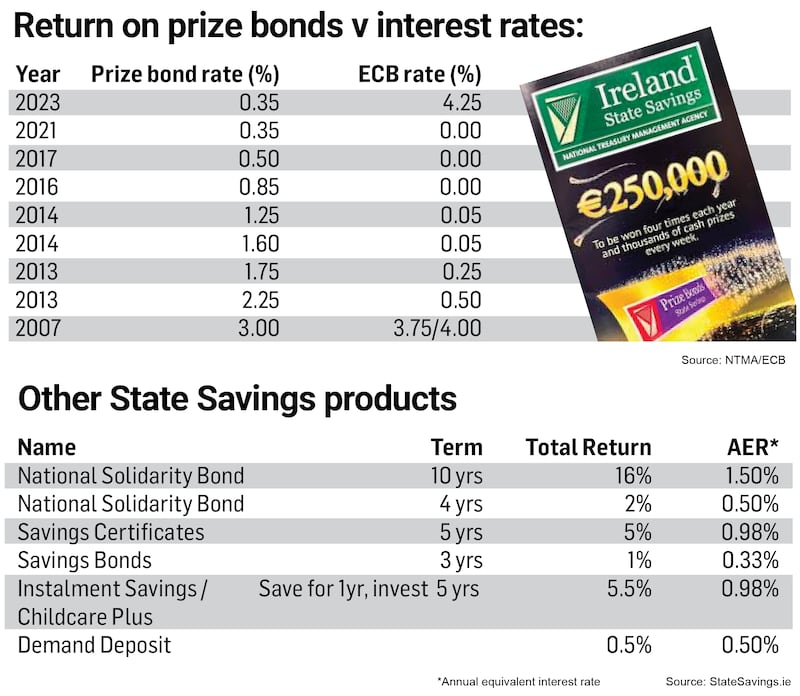

The last increase to the various State savings schemes came in March of this year. At the time of the increase, the NTMA cited the “current interest rate environment” as the reason behind the move. But there were no dramatic increases. The highest AER now available is just 1.5 per cent – and you have to lock your money away for 10 years to get this.

When it comes to prize bonds, beloved by so many, there has been even less action. The interest rate used to calculate the prize bond fund hasn’t been increased in more than 15 years.

So why so little change?

We asked the NTMA. A spokesman responded: “When setting interest rates, the NTMA is mindful of the balance between providing customers with an investment option and providing value to the Exchequer in terms of borrowing costs.”

In other words, Irish savers are a cheap form of funding given their loyalty and preference for deposits – regardless of the return on offer – so why pay them more? He added that the agency is keeping rates under review.

International investors

Of course the same approach isn’t taken when it comes to those more demanding institutional investors. A recent presentation from the NTMA highlighted that it had raised some €13 billion on the bond markets since 2022 at an average interest rate of 2.04 per, cent but this rate is on the rise. In March it sold 10-year bonds at a yield of 3.37 per cent, the highest rate offered in nine years. About half of government bond investors come from continental Europe, with about 22 per cent from the UK.

So why the difference?

According to the spokesman, it is because the “State savings product range is different from Government bonds, and has different product features”, adding that State savings are not subject to Dirt (not that it is substantial given such low returns on offer) while government bonds are subject to tax and have fees and charges associated with them.

Prize bonds

Looking at prize bonds alone, the poor returns on offer are very evident. The last time the rate on prize bonds was changed was way back in 2017 and that was to cut them with the rate sliding from 0.5 per cent to the 0.35 per cent level at which it remains today. That rate is used to calculate the amount paid out in prizes.

Such a low percentage rate comes at a time when the overall inflow to prize bonds is at a record high. Back in 2013, when the prize fund was based on an interest rate of 2.25 per cent, the prize bond fund stood at just €1.9 billion, with a total prize fund of €35.2 million. Last year, the fund stood at a staggering €4.7 billion but, given that prizes were based on an interest rate of 0.35 per cent, just €16 million was paid out in prizes.

So more people own more prize bonds – but the chances of winning and the winnings on offers are considerably lower.

And despite rapid increases in interest rates at ECB level over the past year or so, there has been no move to raise the rate applying to the prize bond fund.

This is in contrast with similar State-run schemes in other countries. In the UK, for example, where the Bank of England rate rose to 5.25 per cent earlier this month, the rate of interest on premium bonds will increase to 4.65 per cent in September from the current level of 4 per cent – the highest since 1999. That will add some £66 million (€77 million) to its prize fund while the odds of winning will move from 22,000 to 1 to 21,000 to 1 – the best level since the April 2008 prize draw.

[ Italy’s bank levy highlights ‘surprising’ lack of pressure in IrelandOpens in new window ]

In France, while no such equivalent to prize bonds exists, there is a State savings scheme – the Livret A – which is available to all French residents and is sold through the banks. It pays a rate of 3 per cent on savings of up to €22,950 following a recent increase. Not so long ago – the start of 2022 in fact – the rate paid on such savings was just 0.5 per cent, so the French government is moving to protect savers against inflation.

Back in 2007, the Irish prize bond fund and the ECB rate was more aligned, with the former paying out 3 per cent against an ECB rate of 3.75/4 per cent that year.

The two actually diverged subsequently in a way that favoured prize bond investors. In 2013, the ECB rate stood at 0.25 per cent but the prize bond fund interest rate was 1.75 per cent. And in 2016, when the ECB rate fell to zero, the prize bond fund was at 0.85 per cent.

It should be noted that this was in the extraordinary circumstances of the time when banks were paying deposit rates of as much as 5 per cent to shore up their balance sheets.